The Income-Related Monthly Adjustment Amount (IRMAA) is an additional charge added to the standard Medicare Part B and Part D premiums for beneficiaries with higher incomes. This adjustment ensures that individuals with greater financial resources contribute more to the Medicare program, aligning their contributions with their ability to pay. Understanding IRMAA is crucial for high-income retirees and those approaching Medicare eligibility, as it directly impacts healthcare costs in retirement.

Understanding IRMAA

Medicare, the federal health insurance program primarily for individuals aged 65 and older, consists of several parts:

- Part A: Hospital insurance covering inpatient hospital stays, skilled nursing facility care, hospice care, and some home health services.

- Part B: Medical insurance covering outpatient care, doctor services, preventive services, and medical supplies.

- Part D: Prescription drug coverage.

While many beneficiaries receive Part A without a premium, Parts B and D typically require monthly premiums. For individuals with higher incomes, IRMAA increases these premiums based on their modified adjusted gross income (MAGI) from two years prior. For example, 2025 IRMAA determinations are based on 2023 income levels.

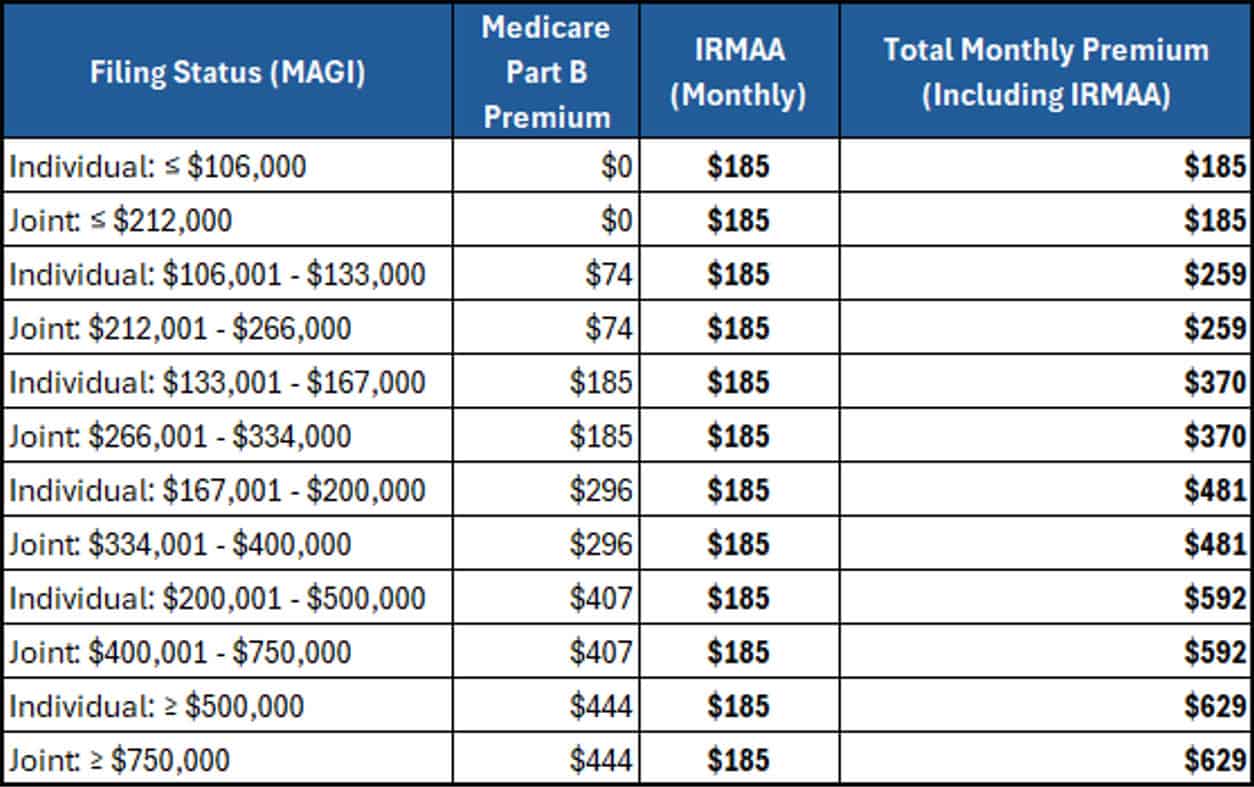

2025 Income Thresholds and IRMAA Brackets

The Social Security Administration (SSA) uses the following income brackets to determine IRMAA for 2025:

2025 IRMAA Brackets and Premiums for Medicare Part B

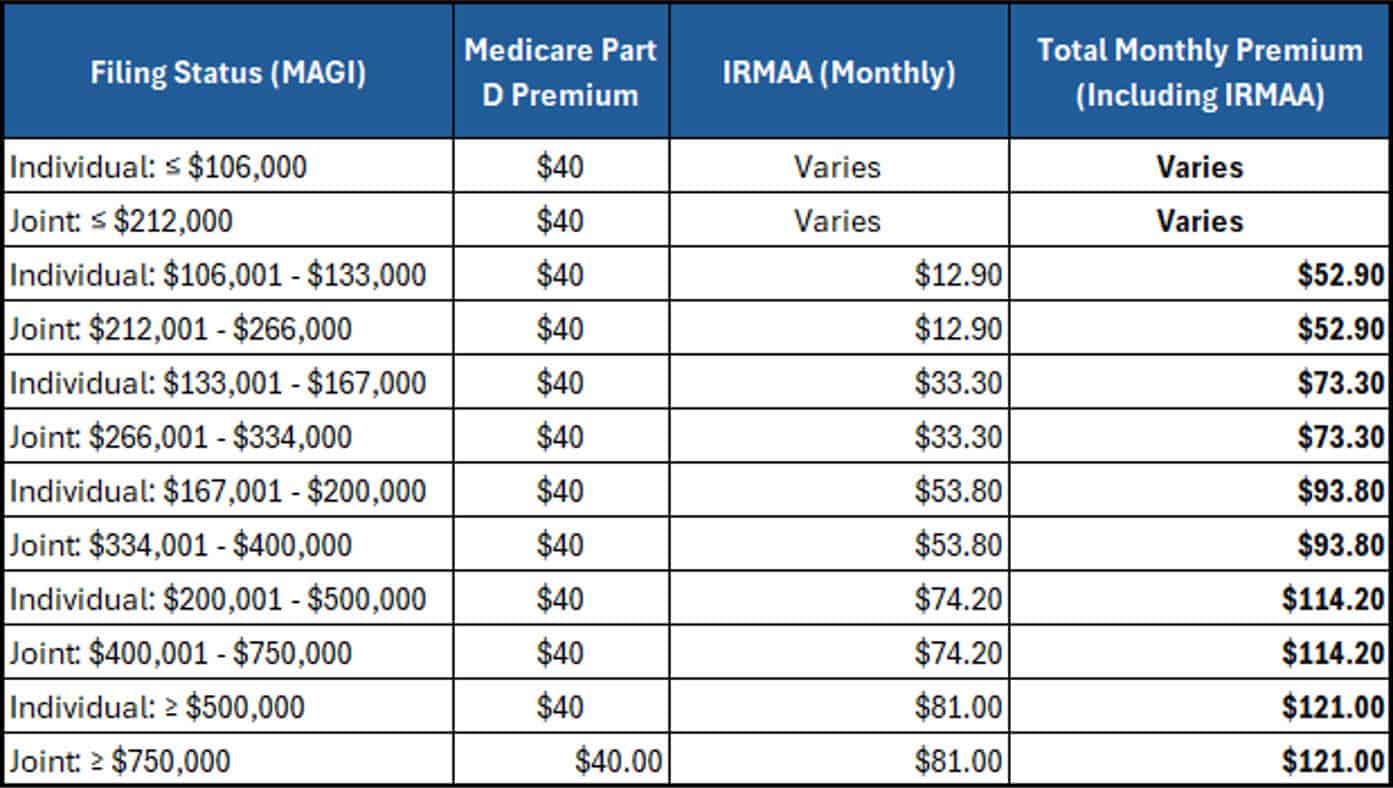

2025 IRMAA Brackets and Premiums for Medicare Part D

(assuming a $40 Medicare Part D premium)

Important Notes:

- Unlike Medicare Part B, Part D premiums vary depending on the specific prescription drug plan chosen by the beneficiary.

- The total premium is calculated as the base plan premium plus the IRMAA surcharge listed in the table above.

- IRMAA for Part D is deducted from Social Security benefits or billed separately by Medicare, not paid directly to the insurance provider.

Pros and Cons of IRMAA

Advantages:

- Progressive Contribution: IRMAA ensures that higher-income individuals contribute more to the Medicare program, promoting equity within the system.

- Funding Support: Additional funds from IRMAA help sustain the Medicare program, potentially enhancing services for all beneficiaries.

Disadvantages:

- Increased Costs: High-income beneficiaries face higher monthly premiums, impacting their retirement budgets.

- Complexity: Understanding and planning for IRMAA can be challenging, especially with income fluctuations and tax considerations.

Hypothetical Examples

Example 1:

John, a single filer, had a MAGI of $120,000 in 2023. In 2025, his Medicare Part B premium would be $259.00 per month ($185.00 standard premium + $74.00 IRMAA). For Part D, he would pay an additional $13.70 per month on top of his plan’s premium.

Example 2:

Mary and Charles, filing jointly, had a combined MAGI of $350,000 in 2023. In 2025, each would face a Part B premium of $480.90 per month ($185.00 standard premium + $295.90 IRMAA). Their Part D IRMAA would be an additional $57.00 per month per person.

Strategies to Manage IRMAA

- Income Planning: Monitor and manage income sources to stay below IRMAA thresholds. This may involve timing income recognition or deferring certain income streams.

- Roth Conversions: Converting traditional IRA funds to Roth IRAs before reaching Medicare eligibility can reduce future taxable income, potentially lowering or avoiding IRMAA.

- Charitable Contributions: Utilizing Qualified Charitable Distributions (QCDs) from IRAs can satisfy required minimum distributions without increasing taxable income.

- Filing Appeals: If you experience a life-changing event (e.g., retirement, divorce), your beneficiaries may be able to appeal IRMAA determinations, potentially reducing premiums.

Conclusion

Navigating Medicare’s Income-Related Monthly Adjustment Amount (IRMAA) is a critical aspect of financial planning for high-income retirees. While it may seem like just another bureaucratic hurdle, the reality is that IRMAA can significantly impact your retirement cash flow. Understanding the income thresholds, potential surcharges, and available strategies to manage or reduce these costs can mean the difference between overpaying for Medicare and keeping more of your hard-earned wealth.

For some, strategically managing income through Roth conversions, tax-efficient withdrawals, or charitable giving can help avoid unnecessary IRMAA surcharges. Others may determine that the benefits of higher taxable income – such as greater investment growth or lifestyle flexibility – outweigh the additional Medicare costs. Either way, knowledge and proactive planning are key.

Ultimately, IRMAA is not just a tax or a penalty – it’s a predictable cost that, when properly managed, can prevent unwelcome surprises and preserve more of your financial security in retirement. By taking control of your income and understanding the rules, you can ensure that Medicare remains a valuable benefit, not an unexpected burden.

Related Articles

What is Medicare?

Financial Planning,

Personal Finance,

January 24, 2024

Why is Income Important in Retirement?

Fixed Income,

Personal Finance,

Top Personal Finance FAQs,

Why to Buy & Where,

August 14, 2024

RMD Timing Secrets: When to Withdraw for Maximum Gains

Behavior,

Investment Principles,

Personal Finance,

Tax,

September 17, 2024