Investors often dread market downturns, viewing them as periods of financial loss and instability. However, institutional direct bond investing offers a unique strategy that not only mitigates risk but also provides significant advantages in a down market. By allowing investors to exercise greater control over their investments, institutional direct ownership creates opportunities for higher yields, steady income, and long-term growth, making bonds an essential component of a resilient portfolio.

Unlike mutual funds or ETFs, which can be subject to forced liquidations and liquidity mismatches during periods of volatility, institutional direct bond ownership provides flexibility and control. Investors can navigate market downturns by strategically purchasing bonds at discounted prices. When bond prices fall, their yields (interest payments as a percentage of the bond’s price) rise, offering higher returns for new investors who lock in these opportunities. In contrast, pooled funds may struggle with liquidity challenges and sell assets at unfavorable prices to meet fund redemptions, leaving their investors exposed to greater risk.

Benefits of Bond Ownership

One of the standout advantages of bonds in a downturn is their consistent income stream. Even as bond prices fluctuate, coupon payments remain fixed, providing reliable cash flow regardless of market conditions. This stability is especially valuable during market sell-offs, where institutional bondholders can reinvest their income to acquire more bonds at lower prices, enhancing their portfolio’s future income potential.

Since bonds are typically less volatile than stocks, their inclusion in a portfolio provides a buffer during turbulent times. This steady income reduces the need to liquidate equities to meet cash flow needs, which is particularly important for retirees or investors relying on consistent income. The predictability of bond payments adds a layer of security that can help stabilize the portfolio when stock markets are under pressure.

Examples of Institutional Direct Bond Benefits

One of the benefits of owning bonds directly is that when bonds go down in value, it doesn’t change the outcome unless the bond or company fails. If prices of bonds go down, whether it’s because interest rates moved up or the bond market declined during a sell-off, your net annual yield, cashflow, and payment at maturity don’t change unless they are sold.

For example, if you invest a million dollars in bonds at a 5% yield-to-maturity, but the bond market declines, the income and the yield-to-maturity don’t change. If you invested in the bonds and the yield-to-maturity is 5%, then even if the bonds temporarily go to $900k in value, the maturity price is still $1M and you are entitled to still receive $50k in annual income.

Benefits of Bond Values Declining

One benefit of bond prices going down is that the bond owner’s buying power increases. As mentioned in the prior example of a 5% bond with $50k in annual income, since income and maturity value don’t change, a decline in the bond market means that you can reinvest the income received at a better price. Much like with dividend stocks, even if the share price goes down the dividend income allows the shareholder to buy more shares at a lower price. The difference is that common stocks don’t have a maturity date or payment at maturity.

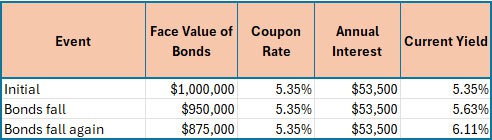

If you own the bonds already, just remember that despite current prices declining, the long-term outcome isn’t affected. What bond market pullbacks do is give the investor the opportunity to buy more bonds with better yields, as you can see below:

Because bond owners have predictable outcomes in yield and principal, they should love when the bond markets move downward. The buying power of their income has been increased. Unlike an equity investor, who has no assurance of income and value, a bond owner can count on the income and payment at maturity so long as the issuer does not default.

In the example above, the investor still receives $53,500/yr even if the face value of the bonds has dropped. Since prices have dropped, the investor can use this income to purchase bonds at lower prices with higher yields. Taking advantage of down markets in this way enhances compounding, potentially creating a faster and more robust recovery from the downturn.

Historically, bonds have shown their resilience in volatile markets. For example, during the 2008 financial crisis, U.S. Treasury yields spiked as bond prices dropped, offering an attractive entry point for new investors. Those who purchased bonds during that period locked in higher yields and reaped the benefits as the market recovered. More recently, in the early days of the COVID-19 pandemic, many bond funds faced massive redemptions, forcing managers to sell bonds in illiquid markets at depressed prices. Institutional direct bondholders, however, avoided these forced sales and the associated losses, maintaining their steady income and control over their holdings.

Financial Advantages of Institutional Direct Ownership

Beyond stability, institutional direct bond investing offers notable financial advantages. The consistent income generated from bonds allows investors to reinvest at lower prices, effectively using discounted dollar-cost averaging to increase their bond holdings or diversify into equities. This approach can magnify long-term gains, particularly in a down market where opportunities to buy discounted assets abound.

Institutional direct ownership also enhances tax efficiency. Investors can capitalize on strategies like gifting appreciated bonds or employing tax-loss harvesting to offset gains in other areas of their portfolio. Moreover, institutional direct bond investing generally comes with lower costs compared to bond funds, which often carry management fees and other expenses that can erode returns.

Behavioral and Portfolio Stability Benefits

One of the less-discussed but important benefits of institutional direct bond ownership is its influence on investor behavior. By removing the need to react to the behavior of others in pooled funds, where investors may redeem shares en masse during volatile periods, institutional direct bondholders can make more rational, long-term decisions. This independence allows investors to avoid the herding effects and forced liquidations that can drive fund prices even lower.

Furthermore, institutional direct bondholders retain full control over their investment strategy. They can decide when to buy or sell based on market conditions, without the influence of external fund managers. During downturns, this control becomes even more valuable, as it enables investors to act opportunistically and take advantage of market dislocations.

Risks to Consider

While institutional direct bond investments offer numerous benefits, it’s important to acknowledge the risks. Default risk is the possibility that a bond issuer may fail to make interest or principal payments. While companies are required to pay out bondholders before shareholders in the event of a default, a company failure could leave an investor with worthless bonds.

Additionally, rising interest rates can affect the resale value of bonds on the secondary market. When interest rates increase, existing bonds with lower rates become less attractive, which could impact demand and the bond’s market price. However, investors who hold bonds to maturity can avoid these risks and continue receiving their fixed coupon payments and principal repayment.

Long-Term Wealth Accumulation

By reinvesting the income from bonds and dividends, institutional direct bond investors can accumulate more assets at discounted prices, setting the stage for substantial gains when the market rebounds. This strategy is particularly effective for long-term investors who have the patience to weather short-term volatility in pursuit of compounding returns. Institutional direct ownership not only helps investors maintain control during down markets but also positions them to capture future growth potential by reinvesting income into undervalued bonds or stocks.

Institutional direct bond investing offers a powerful combination of stability, control, and long-term financial benefits, especially in times of market downturn. The ability to lock in higher yields, reinvest income, and tailor bond holdings to individual goals makes this strategy an essential tool for both income generation and capital growth. By removing the risks associated with pooled funds and maintaining full control over investment decisions, institutional direct bondholders can navigate volatile markets with confidence, while building a stronger, more resilient portfolio designed for the future.