Index funds, advertised as low-fee options, are popular investment vehicles for long-term investors. They track market indices such as the S&P 500, making them an attractive option for diversified equity exposure. However, during down markets, these funds reveal certain drawbacks that investors should consider.

No Downside Protection

Because there is no focus on the quality of holdings, index funds offer no protection against falling markets. Since they are passively managed, they don’t adapt to market conditions or reduce exposure to declining sectors. This lack of consideration for quality can leave investors vulnerable to steep losses, especially during prolonged bear markets or recessions.

Delistings, or the removal of stocks from an index, can have a considerable impact on index performance. A company can be delisted from an index for several reasons, such as a merger, acquisition, bankruptcy, or failure to meet listing requirements. When a shrinking company falls below the requirements it is removed from the index, but the value lost before delisting is permanent.

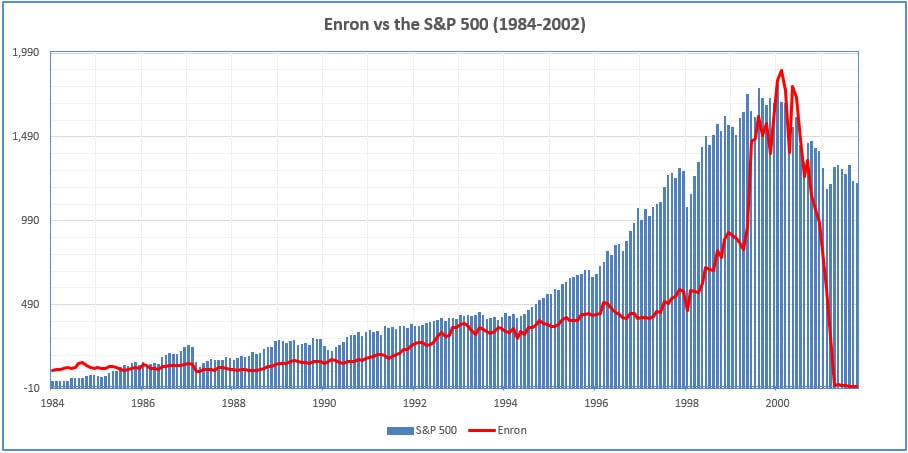

Enron’s delisting in 2001 is good example of why only considering a company’s size can be perilous. Once a darling of Wall Street, the company was a major constituent of the S&P 500. When its accounting fraud was uncovered and the stock price collapsed, index funds holding Enron suffered immediate losses. Enron was only removed from the S&P 500 index a few days before filing for bankruptcy, meaning the index did not reconstitute in time to prevent index investors from suffering losses.

When a company like Enron is delisted after significant losses, investors lose most (if not all) of the money allocated to that company. This can make a full recovery nearly impossible. Why is this important to investors? If a company in a pooled market-cap index fund loses all or most of its value, then the companies that remain must work harder to recover the value lost. Recovering from a down-market means that you recover your principal and begin to make money again. Recovery restores your compounding. Because recovery from down-markets is critical to long-term compounding, the importance of earnings quality within an index can’t be overstated.

A few other examples of companies that failed while in market-cap index funds are General Motors, Washington Mutual, and Lehman Brothers. While these companies may have only represented a relatively small percentage of an investor’s portfolio, their failure can significantly impact the portfolio’s ability to recover.

(Source: Factset) Investors cannot invest directly into an index.

Exposure to the Entire Market Decline

One major drawback of index funds during market downturns is that they are designed to mirror the performance of an index. When the market declines, the value of an index fund follows suit. This can result in significant losses if the broader market or specific sectors within the index suffer substantial downturns.

Concentration Risk

Although index funds are typically well-diversified, some can have concentrated exposure to specific sectors or stocks, especially in indices like the S&P 500, which is heavily weighted toward large-cap technology companies. In a market downturn, if these heavily weighted sectors perform poorly, the index fund can suffer substantially.

Slow Recovery Compared to Quality-Focused Strategies

In a market recovery, index funds will rise in line with the overall market. However, they may not bounce back as quickly or as strongly as quality-focused strategies. Screening companies for quality allows investors to remove companies that are likely to be a drag on performance and recovery.

There are some instances where a company has been delisted from an index and removed from index funds but ends up recovering in the long-run. Investors in pooled funds did not have the opportunity to hold these companies and recover their value.

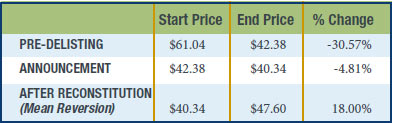

AutoNation was removed from the S&P 500 index in 2017 due to the company’s declining market capitalization and performance relative to other firms in the index. Companies that see their market cap shrink below a certain threshold relative to others may be removed to maintain the index’s representation of the largest U.S. firms. Despite being a well-known auto retailing brand, a declining market cap relative to peers resulted in AutoNation’s deletion from the S&P 500 in 2017. This removal signaled a rough patch for the company, which faced pressure to evolve in a rapidly changing market environment.

Source: Factset

As you can see in the above table, after being delisted AutoNation quickly recovered much of its value. By late 2020 AutoNation had recovered completely, and as of 10/14/2024 was priced at $167.27 (nearly 3 times its pre-delisting price). Investors in an S&P 500 index fund would only participate in AutoNation’s decline, not its recovery.

This process is known as reverting to the mean. This can be a big challenge for mega-sized market-cap index fund companies. When a company is delisted, the volume of sales on the stock is overwhelming due to the volume of assets being managed by the fund company.

Earnings Focused vs. Market Capitalization

With the creation of earnings-quality focused institutional indexes through Linden Thomas & Co. and our sister company, Indexperts, investors can move from pooled ownership of assets to direct ownership and build their portfolio based on earnings-quality rather than market capitalization. Why is this important? Because quality and ownership matter!

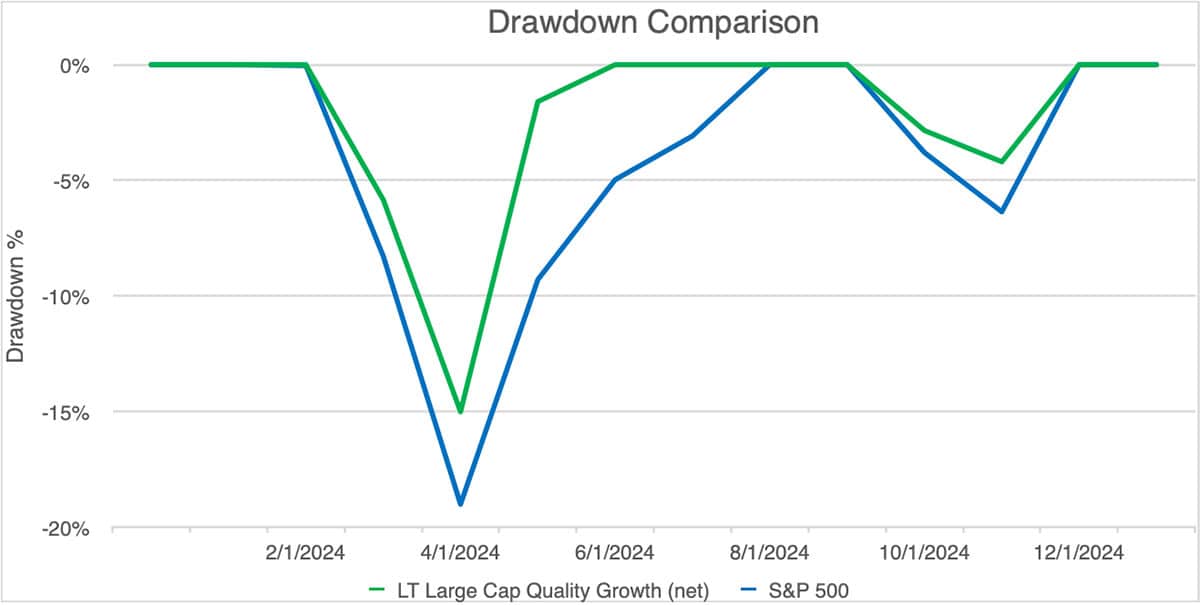

Many companies lost nearly their entire value due to the 2020 COVID pandemic. A few examples are Earth Fare, JC Penny, Century 21, and Brooks Brothers. When companies lose their total value, the recovery of one’s portfolio is much more difficult. When one owns companies directly that are screened for earnings quality, the probability of recovery is enhanced. The importance of earnings quality can be seen clearly when comparing the S&P 500 (market-cap based) and one of Linden Thomas & Co.’s earnings focused institutional indexes, specifically the Large-Cap Quality Growth.

(Source: Zephyr) Investors cannot invest directly into an index. Past performance is no guarantee of future results.

As you can see above, both the S&P 500 and the earnings-focused Linden Thomas & Co. Large-Cap Growth Index declined during the down-market. However, the earnings-focused index didn’t fall in value as much as the S&P 500 and recovered two months sooner. While index funds spread risk between many holdings and have a lower minimum investment required, these results show that quality and direct ownership can have a big impact on results and recovery.

With institutional direct indexing, investors can customize their portfolio, allowing for greater control and flexibility. This means that during a market downturn, investors can strategically sell underperforming stocks, harvest tax losses, or adjust exposure to specific sectors that they believe will recover more quickly. Additionally, direct indexing enables investors to tailor their portfolio to align with personal values or financial goals, potentially offering more targeted downside protection than a standard index fund. By evaluating the earnings-quality of the companies in the index, direct indexing investors can add another layer of confidence to their investment strategy.

While index funds advertise simplicity and low fees, their performance during down markets can be less favorable due to their inability to avoid or mitigate losses. Investors should weigh these drawbacks and consider their risk tolerance, particularly during periods of market volatility.

Related Articles

Building a portfolio with a correction in mind vs timing the correction

Investment Principles,

Markets,

Portfolio Considerations,

October 1, 2024

The Market Is Like a Coin—It Has Two Sides: Up and Down

Investment Principles,

Knowledge & Insights,

Markets,

Understanding Results,

September 17, 2024

Why Are Down Markets Your Friend?

Behavior,

Investment Principles,

Markets,

November 19, 2024