By Indexopedia Research Team | October 1, 2024 | In

Today, many investors are gripped by the fear that the market is overvalued and poised for a correction. But history teaches us that trying to time the market is not only difficult–it can be disastrous. Instead, we believe a balanced, well-constructed portfolio that focuses on spreading risk is key to long-term success. One such approach is the classic 60/40 portfolio, where 60% of assets are allocated to stocks and 40% to bonds.

Why Predicting the Market is a Fool’s Errand

The stock market has a long history of reaching new highs. It’s often at these peaks that investors become wary, convinced that a correction is imminent. While it’s true that corrections and downturns are part of the market’s natural cycle, predicting their exact timing is virtually impossible. Market momentum can persist for years even if you think they’re overvalued, and even when a downturn occurs, knowing when to re-enter is equally challenging.

Take, for example, an investor who sold their stock holdings in 2013, believing the market was due for a correction after strong gains post-2009. They sat in cash, waiting for a downturn that never arrived, missing out on one of the longest bull markets in history!

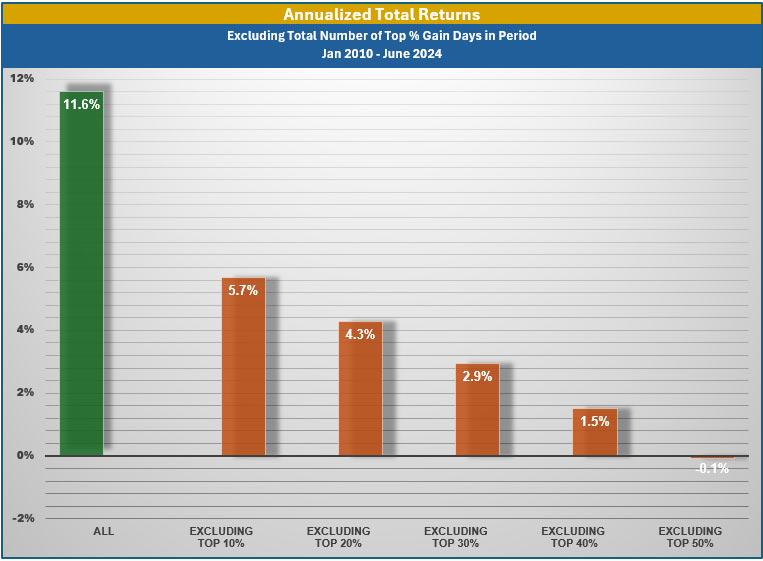

The risk of missing the best days in the market is real. According to research by J.P. Morgan, from 1999 to 2018, the S&P 500 provided an average annual return of 5.62%. But if an investor missed just the 10 best days in that period, their return would have dropped to a mere 2.01%. The market’s best days often follow its worst, which is why trying to time the market can severely damage long-term returns.

Exhibit 1: (Source: Factset)

The 60/40 Portfolio: A Balance of Risk and Reward

A 60/40 portfolio–60% in stocks and 40% in bonds–offers an ideal balance for moderate investors who want to manage risk while staying invested in both the equity and fixed-income markets. This allocation is particularly suited for those who are concerned about potential market volatility but still want exposure to the growth opportunities that stocks provide.

1. Bonds as a Stabilizer:

The 40% allocation to bonds provides a steady income stream and acts as a cushion during stock market downturns. These instruments tend to be less volatile than stocks, and during periods of market stress, bonds can increase in value as investors seek safer assets. This stabilization allows the portfolio to weather market storms without introducing excessive volatility.

2. Stocks for Growth:

The 60% allocation to stocks ensures the portfolio still participates in the long-term growth potential of the domestic economy. While it’s true that stocks are more volatile than bonds, over time they tend to provide higher returns, contributing to the portfolio return. The 60% exposure to equities strikes a balance between capturing some of that growth potential while reducing the risk that comes with a 100% stock portfolio.

By keeping the stock allocation at around 60%, investors are able to stay in the market without being overly exposed to its ups and downs. This allocation helps reduce emotional reactions to short-term market movements, like panic selling during a downturn, which can derail long-term success.

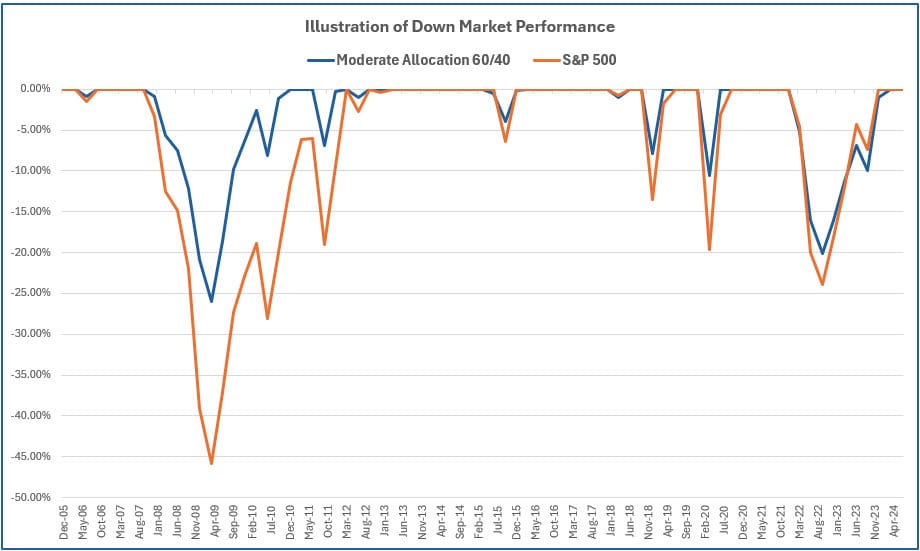

Exhibit 2 below is a down-market comparison of the S&P 500 versus a 60/40 over a roughly 19-year period (including the Great Financial Crisis). It clearly shows how significantly the blended portfolio outperforms the straight stock portfolio during periods of greatest volatility (eg: the GFC of 2008-09).

Exhibit 2: (Source: Zephyr. An index is unmanaged, and you cannot directly invest in an index)

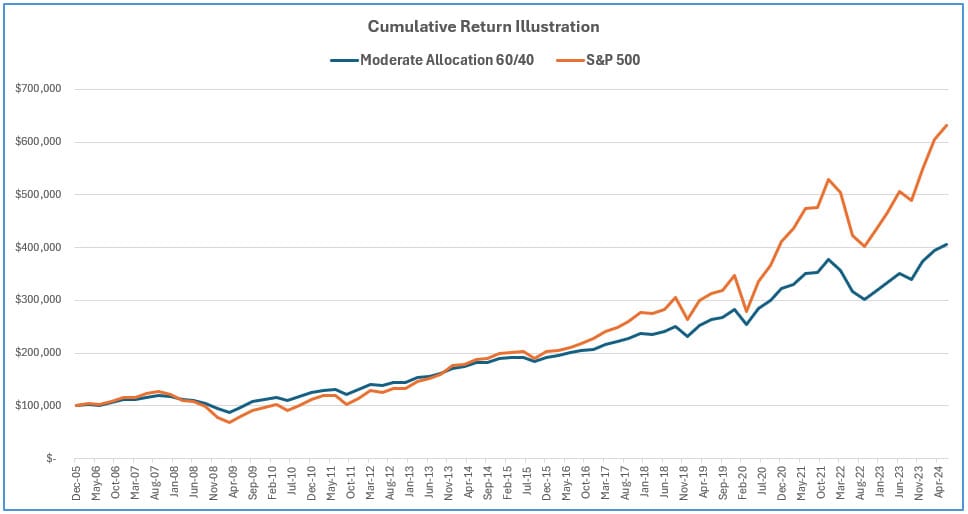

The performance of a 60/40 portfolio may lag a portfolio of 100% stocks over a long time horizon, but the ability to provide investors with the additional financial cushioning may be worth the potentially lower returns. Below is a chart (Exhibit 3) which illustrates how a hypothetical 60/40 portfolio would have performed against a straight 100% investment in stocks over the roughly 18-year period of 2006-2024:

Exhibit 3: (Source: Zephyr. An index is unmanaged, and you cannot directly invest in an index)

The Power of Staying Invested

The key to success with a 60/40 portfolio, like with any strategy, is staying invested through market cycles. Time in the market is more important than timing the market. History has shown that markets are unpredictable, but they tend to rise over the long term. By remaining invested, even when the market seems overvalued or when downturns seem imminent, investors ensure they don’t miss the recovery.

For example, let’s look again at the Great Financial Crisis of 2008-2009. Investors who sold their stock holdings at the bottom in early 2009 missed out on one of the most dramatic recoveries in modern history. Those who remained invested saw their portfolios recover and grow significantly in the subsequent years. The 60% bond allocation in this scenario would have provided enough stability to minimize the pain during the crash, while the 40% in stocks would have captured the growth in the recovery.

Exhibit 4 illustrates how much return would be forfeited if an investor had missed the top 10, 20, or 30 days of the recovery associated with the Great Financial Crisis.

Exhibit 4: (Source: Factset)

Warren Buffett’s Wisdom Applied to a Balanced Portfolio

Warren Buffett’s famous advice–“be fearful when others are greedy, and greedy when others are fearful”–perfectly aligns with the philosophy behind the 60/40 portfolio. When markets are climbing to new highs, it’s tempting to chase stocks and go all-in, just as it’s tempting to run for the exits during market downturns. But a balanced portfolio helps investors stay rational.

The 60/40 allocation ensures that when others are being greedy, the majority of your portfolio is in the safety of bonds. Conversely, when others are fearful and the stock market is falling, the bond allocation protects the portfolio while the stock allocation allows you to remain invested and potentially add to your positions at lower valuations, effectively capturing long-term growth potential.

Real-Life Application: The Pandemic Market Crash and Recovery

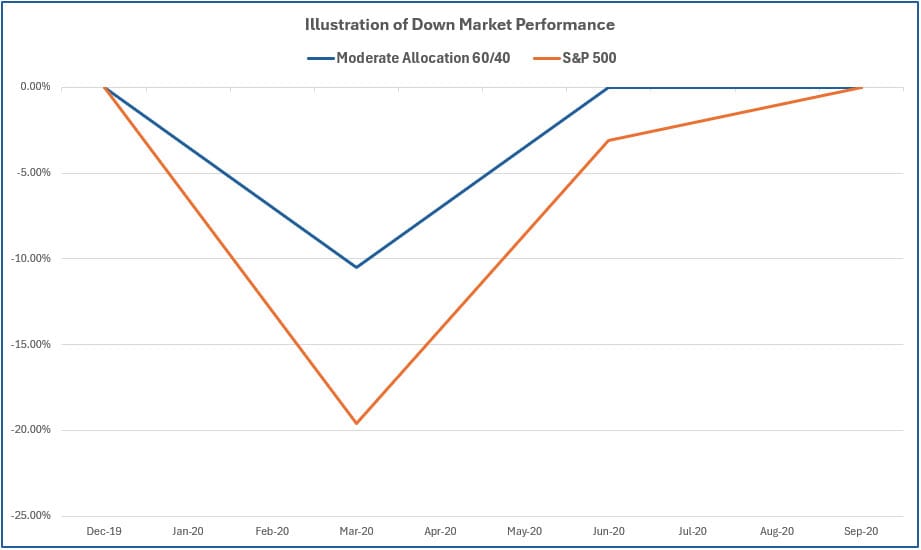

A real-world example of the benefits of a 60/40 portfolio is the market crash during the COVID-19 pandemic. In early 2020, the stock market plunged by over 30% in a matter of weeks. Investors with 100% stock portfolios saw their values plummet, while those with a 60/40 allocation experienced significantly less volatility.

As the recovery began later in 2020, the stock portion of the portfolio rebounded, providing growth, while the bond portion continued to offer stability and income. Investors who stayed the course through the volatility, instead of trying to time the market, reaped the rewards of a balanced approach (see Exhibit 5).

Exhibit 5: (Source: Zephyr)

Managing Risk in the Face of Market Highs

Even when the market is at an all-time high, trying to predict a downturn is a fool’s errand. Instead, we believe focusing on managing risk is a better strategy. A 60/40 portfolio offers a way to do just that, providing the comfort of bond stability while still allowing for participation in the long-term growth potential of the stock market.

By allocating 40% to bonds and 60% to stocks, investors can remain calm during periods of volatility, avoid the emotional pitfalls of market timing, and give themselves the best chance for long-term success. Remember, the goal is not to predict the market but to build a portfolio with a focus on earnings quality, direct ownership of shares, and controlling costs while also spreading risk between sectors and asset classes.

Related Articles

Why Are Down Markets Your Friend?

Behavior,

Investment Principles,

Markets,

November 19, 2024

How Down Markets Can Actually Benefit Investments in Bonds and Dividend Stocks

Behavior,

Fixed Income,

Investment Principles,

Markets,

Why to Buy & Where,

August 14, 2024

If Down-Markets are Normal, Why Should I Invest?

Markets,

Top Markets FAQs,

January 8, 2025