Investing during volatility can feel like running toward a fire when everyone else is sprinting away. But counterintuitive as it may be, history shows that down markets tend to recover and reward those who bought through the pain.

Of course, it’s one thing to say “buy the dip” and another to actually formulate a disciplined strategy to pinpoint opportunities and mitigate timing risk.

In this piece, we’ll not only discuss the challenges of market volatility but also compare three common responses to a downturn — buying more, doing nothing, and fully liquidating — and show how each has played out over the last couple of decades.

The Emotional Toll of Volatility

Portfolios are personal. They’re a numerical representation of your hard work, patience, and planning. Consequently, market pullbacks sting because they directly impact your financial life.

And when fear creeps in, the implse to act — to do something — can be overwhelming.

That’s the emotional tax of volatility. Humans are wired to avoid pain, and when markets tumble, retreating can feel like the only rational response. That said, the flight-or-flight instinct typically leads to costly decisions.

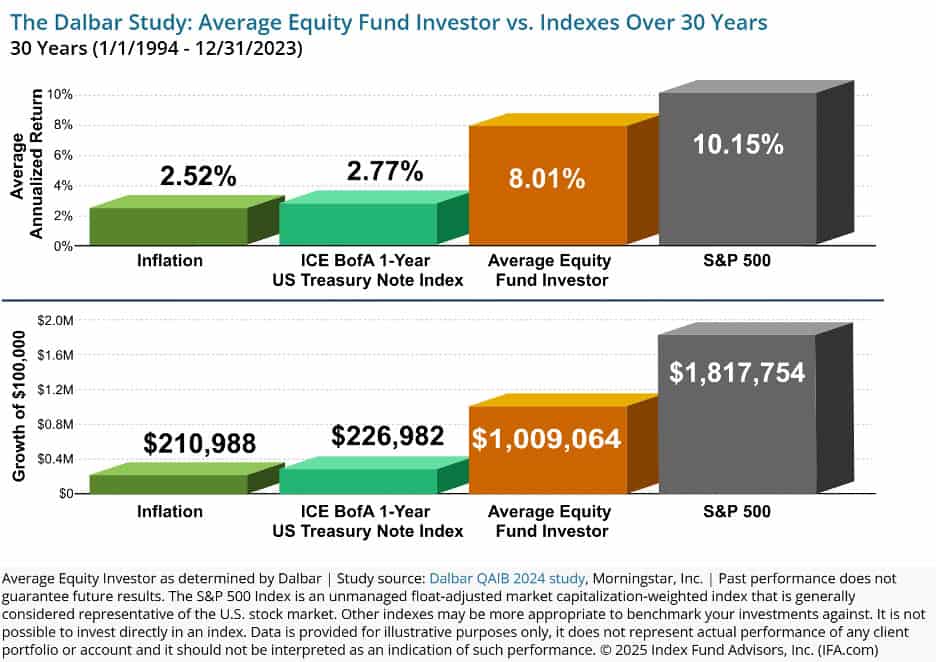

Research consistently shows that investors underperform the very funds they invest in, largely due to poor, emotion-driven timing decisions. One notable study from Dalbar found that over a 30-year period, the average equity investor (8.01% average annual return) significantly lagged the broader market (10.15%).

It doesn’t help that many of the market’s best-performing days tend to happen shortly after the worst ones (e.g., the dot-com bubble, 2008 financial crisis, COVID-19 pandemic). Missing those critical rebound moments can cause long-term results to suffer: if you missed the top 10 trading days over the last 30 years, your return would have been reduced by 54%.

Three Paths Through a Pullback: Real-World Comparison

There are three routes investors typically take when markets drop: buying, holding, and selling.

With this in mind, let’s relive the 2008 financial crisis, one of the steepest declines and financially unstable times in modern markets.

This disruptive period was triggered by a collapse in the housing market, fueled by excessive leverage and risky mortgage-backed securities. Major institutions like Lehman Brothers failed, credit markets froze, and consumer confidence plummeted. The S&P 500 fell about 57% from its peak, and the US economy entered the deepest recession since the Great Depression.

Assuming this environment, we’ll explore the long-term return implications of three approaches:

- Scenario A: Stay invested and maintain portfolio contributions despite the turmoil.

- Scenario B: Liquidate all positions and temporarily stop portfolio contributions.

- Scenario C: Stay invested but stop portfolio contributions altogether.

We’ll assume three $500,000 portfolios were invested at the same time at the end of 2005, and that each mirrors the performance of the S&P 500 and ignores any tax consequences.

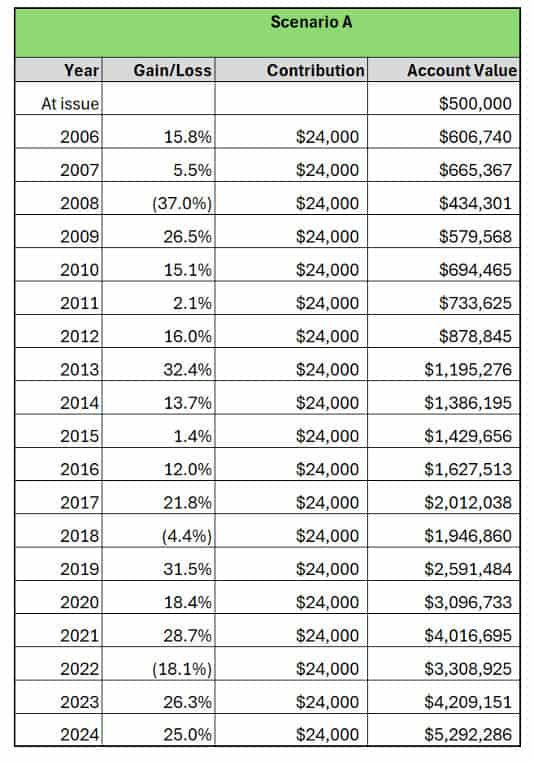

Scenario A

Leading up to the Great Recession, the portfolio peaks at just over $665,000. By the end of 2008, the portfolio falls to $434,301 — despite $72,000 of contributions to date ($2,000 per month).

While easier said than done, this portfolio rides out the volatility with dollar-cost averaging and a long-term perspective. Over the ensuing decade and a half, the account appreciates substantially to $5.3 million.

This outcome underscores the power of staying invested and consistently contributing during downturns, even when it feels uncomfortable.

(This example is for illustrative purposes only and should not be interpreted as representative of any actual client portfolio’s results)

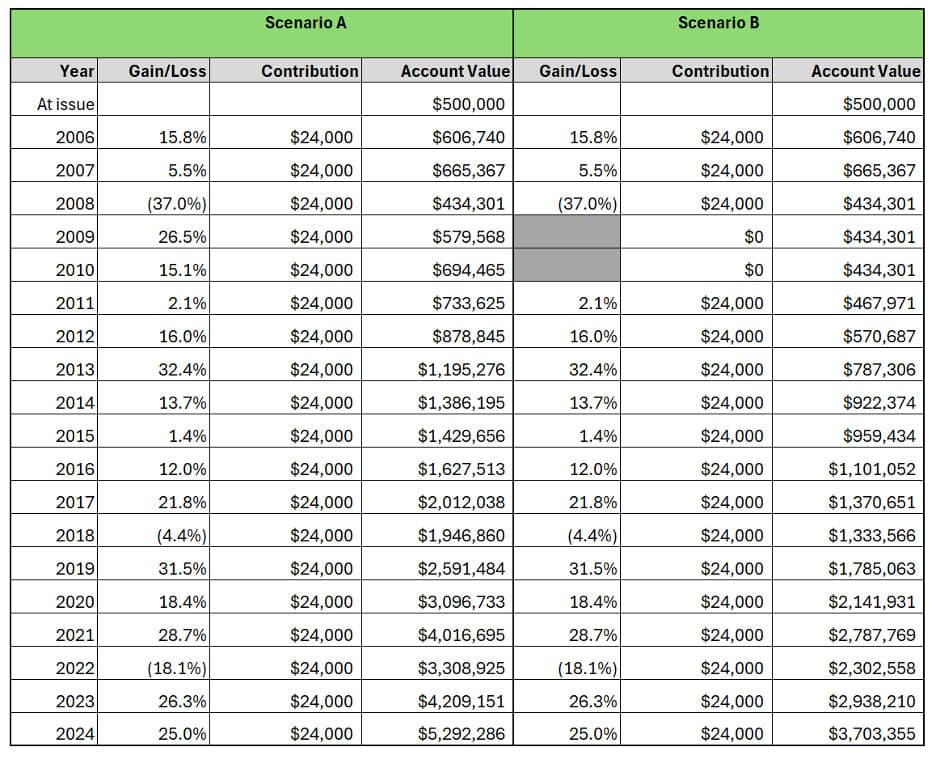

Scenario B

2008 was a distressing time for nearly every investor. Retirement accounts were cut in half, headlines warned of systemic collapse, and major banks were teetering on the edge of insolvency. For many, the fear of further loss overrode long-term strategy; moving to cash felt like the only safe option.

In this scenario, the portfolio is liquidated at the end of 2008 — not long after the market’s bottom.

Untrusting of markets and the financial system as a whole, this investor remains sidelined for two years, resuming contributions at the beginning of 2011. As a result, they avoid another six months or so of volatility, but they also miss the initial rebound.

Even though this portfolio receives regular contributions from 2011 onward, the final account value is $3.7 million by the end of 2024; while still solid, it’s roughly $1.6 million less than the first scenario’s balance.

This example is for illustrative purposes only and should not be interpreted as representative of any actual client portfolio’s results)

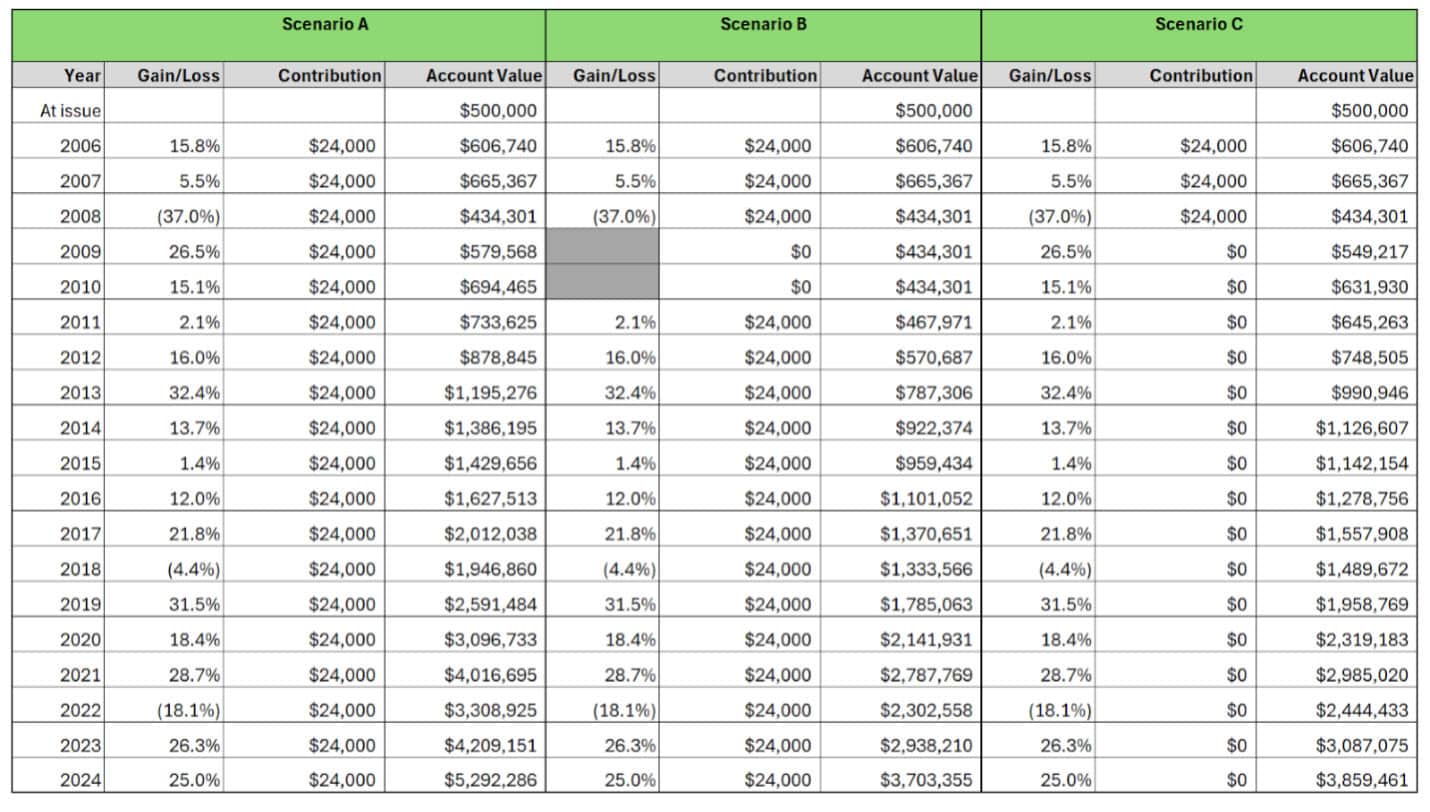

Scenario C

Our final scenario is arguably the most interesting result. Halting contributions indefinitely is as unlikely as it is ill-advised. That said, thanks to holding firm and not selling amid volatility, this portfolio doesn’t lock in losses and, instead, benefits from the initial rebound.

So much so that it actually outperforms the portfolio in Scenario B by about $156,000 — even with a contribution shortfall of $336,000.

While pausing contributions hindered the portfolio’s compounding power, simply staying invested helped this investor avoid the most detrimental outcome: missing the market’s strongest recovery stretch.

(These examples are for illustrative purposes only and should not be interpreted as representative of any actual client portfolio’s results)

Why Buying When It Hurts Tends to Work

Market corrections are a natural (and inevitable) part of investing. On average, markets have experienced one correction of at least 10% per year since 1928. And bear markets (losses of at least 20%) occur every three years or so.

While they can feel unnerving in the moment, history shows that corrections and downturns have consistently been followed by recoveries. Consequently, volatility may create opportunities. During periods of fear and forced selling, high-quality companies and assets can become significantly undervalued.

It’s one thing to talk about “buying low” though. It’s quite another to practice it when headlines are blaring about layoffs and recessions. That’s because humans are inherently ill-equipped to be good investors due to psychological biases, such as loss aversion, herding, and recency bias.

The key is remembering that these emotions are normal. They just aren’t good investing guides. Long-term investors who maintain discipline during pullbacks — or better yet, added to their portfolios — tend to be rewarded as markets recover.

How to Manage the Pain

When you break a bone or strain a muscle, pain management is difficult. The immediate instinct is to seek relief — but sometimes, pushing through discomfort is part of the healing process.

The same is true for investing. Volatility is painful in the moment, but staying the course can be critical for long-term growth. Here are a few strategies that can help you endure the temporary aches and retain sight of the bigger picture.

Set Up Automated Investing

Automatic contributions and periodic rebalancing can help take emotion out of your investment decisions. By committing to a set schedule (regardless of market conditions), you’re more likely to buy when prices are lower and maintain investment discipline.

Use a Rules-Based Investment Plan

A written plan outlines how you invest, diversify, and rebalance — as well as how you’ll respond to market declines. This could include setting asset allocation targets, using specific criteria to select or monitor investments (like valuation or long-term performance), and rebalancing your portfolio when allocations drift beyond set thresholds.

Work With a Financial Advisor

Fear and doubt are heavy emotions to bear during downturns. A trusted advisor can provide perspective, helping you stick to your strategy, evaluate new opportunities, and prevent reactionary decisions that could delay your long-term goals