Learning How Early Saving Empowers Result

All too often investors get lost chasing the best return, when what is most important is actual savings. Those who save a little over long periods of time often don’t need to chase returns, because half of meeting retirement goals is the savings. Yes, returns are the other half, but if one does not save until they are older, the shortfall can be significant.

Meeting one’s retirement goals has two factors, like 1 + 1 = 2. Well, savings + returns = healthy retirement! If you add savings over a long period of time with returns, then a bountiful retirement is in store. Saving early and doing it over a long period of time makes for great stories. But those who put off saving–replacing saving with spending–often get used to a lifestyle they can’t afford when they get older.

In fact, one common misconception is, “I’ll spend now while I’m still young and can enjoy it.” Well, it sounds good, but when you’re in your 50s–or worse, late 60s–and you have to work because you can’t afford to retire, this is tragic. Bragging about what you have now, only to lose it when you should be slowing down, is no way to live.

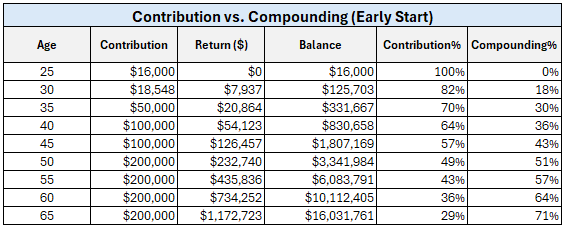

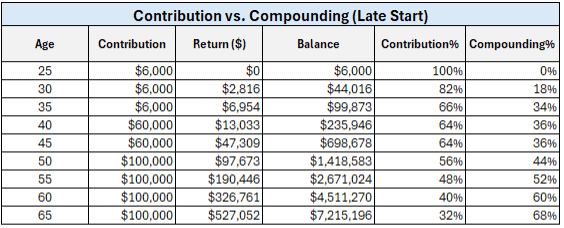

So, let’s look at three examples of a saver. All three are professionals with the same income, with salaries moving up to the point that they all earn $600,000 per year by the time they are 50. At the age of 25, Saver A saves $16,000 a year (or $1,333 per month) and gradually moves savings to $200,000 a year from age 50 to 65. Saver B starts saving $6,000 a year and moves saving up to $100,000 a year to the age of 65. Notice that Saver A’s compounding becomes 50% of the total value at age 49, while Saver B’s compounding doesn’t become larger than their savings until age 55.

These are hypothetical returns and time periods shown are included strictly for illustrative purposes. These returns are not reflective of any investment strategy by the investment adviser nor are they the results of any client account managed by the adviser.

These are hypothetical returns and time periods shown are included strictly for illustrative purposes. These returns are not reflective of any investment strategy by the investment adviser nor are they the results of any client account managed by the adviser.

One thing many investors fail to understand is that, as an investor, you eventually want the money to work harder than you do. Saving early with a balanced approach goes a long way toward getting there. At the age of 65, Investor A, at a 4% distribution rate, turns savings into $640,000 in annual income, while Investor B will earn $288,000 per year. Investor A now has an equivalent income to what they earned while employed, while Investor B fails to earn even half of that.

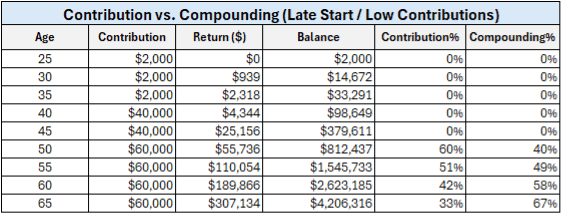

Now let’s look at Saver C below. This, unfortunately, is ugly–and yes, it does happen. This investor saves half of what Saver B saved. As you can see, by the time they turn 65, at a 4% distribution rate, they only have $144,000 per year. If you’re used to earning $600,000 a year and now earn less than a quarter of that, the challenge is that you’re downsizing significantly just to survive.

These are hypothetical returns and time periods shown are included strictly for illustrative purposes. These returns are not reflective of any investment strategy by the investment adviser nor are they the results of any client account managed by the adviser.

All too often, these “no savers” seek out higher returns, which means more portfolio risk during a time they should be scaling back risk, and seldom does chasing returns work.

Compounding is made up of three factors: savings, portfolio results, and time. Portfolio returns are also made up of three factors: upside capture, downside capture, and down-market recovery (link: https://stg.indexopedia.com/3-factors-of-compounding-upside-downside-and-recovery/). If you seek higher returns, this often comes with higher downside risk and delayed down-market recoveries. Increasing down-market risk before or during retirement can–and often does–end in disaster.

So, if you have the benefit of age and many years ahead of you, consider this: you want your money to work harder than you the last half of your life, but it can’t unless you work harder and save the first half of your life. Save now and have it later!

Related Articles

Your Investments Can’t Save You: How Poor Financial Habits Destroy Retirement Dreams

Personal Finance,

March 28, 2025

Frugal, yet Wealthy: Luxury Today, Poverty Tomorrow: A Cautionary Tale

Personal Finance,

June 11, 2025

How to Start Saving for Retirement

Financial Planning,

Investment Principles,

Personal Finance,

Top Investment Principles FAQs,

May 14, 2024