The removal of pooled fund inefficiencies, combined with the insights and education provided by our team, allows investors to be confident in their portfolio. However, even with an efficient portfolio, investors can still be unhappy due to four factors:

- Poor Portfolio Construction

- Lack of Insight and Understanding

- Poor Investor Behavior

- Poor Support

Poor Portfolio Construction

The first reason investors can be unhappy is due to poor portfolio construction. This is seen often with retail investment advisors who are limited by their experience, technology, products, licensing, and/or team support. These advisors use third-party, pooled products that have several drawbacks.

- Hidden costs of investment products

Such as expense ratios and internal trading costs. - High investment advisor fees

Some investment advisors charge 1% or more, not including the costs of the products they offer. - Portfolio Overlap

Unintentional overlap in sectors or holdings within investment products can lead to overconcentration of underperforming assets or include more downside risk than investors desire. - Low-Quality Holdings

Portfolios could include securities of companies that are unhealthy, often making them speculative or high-risk. - Low-Yielding Bonds

Low-yielding bonds are often found in bloated pooled bond funds. Carrying these bonds with pricing disadvantages and low yields only adds to the damage of internal trading costs and hidden fees. Low yield bonds can be especially painful for retired investors in need of net cashflow.

Lack of Insight and Understanding

Lack of insight or understanding can often lead to poor investor satisfaction, even if the portfolio is constructed efficiently. Making bad comparisons, not understanding the tradeoff between risk and reward, and focusing too much on short-term results, can leave investors disappointed in their portfolio.

- Bad Benchmark Comparison

If one compares a balanced portfolio (a mix of several asset classes, equities and bonds) to a single sector, like large-cap stocks (the S&P 500, for example), they may be disappointed when large-cap stocks are doing well. Comparisons like this can be especially confusing for the uninformed, because recent results will be reflected in the trailing average returns. - Not Understanding Risk vs. Reward

Not all risk is rewarded, but historically aggressive investors with a high-risk tolerance can end up with better results over long periods of time. However, returns at any given point in time are not necessarily an indicator of long-term success. For example, an investor who is near retirement and needs income might have a balanced portfolio with limited exposure to growth equities. If the investor compares their approach to a portfolio with limited bond exposure and a focus on growth stocks, they may be inclined to change strategies. This could be a catastrophic mistake when the markets take a turn and risk taking is punished. - Focusing Too Much on Short-Term Results

In the short-term the stock market may not recognize the quality of a company’s earnings, but in the long-term it does. Public companies that trade on the NYSE or the NASDAQ may go up and down, but ultimately stocks with poor earnings can only survive so long. While high returns in certain sectors can seem promising, it’s always a good idea to review portfolio quality.

Bad Investor Behavior

A lack of understanding often leads investors to make bad decisions. Without understanding how sectors and assets rotate into and out of favor over time, investors could end up chasing fads and losing progress.

- Average Return Impacts

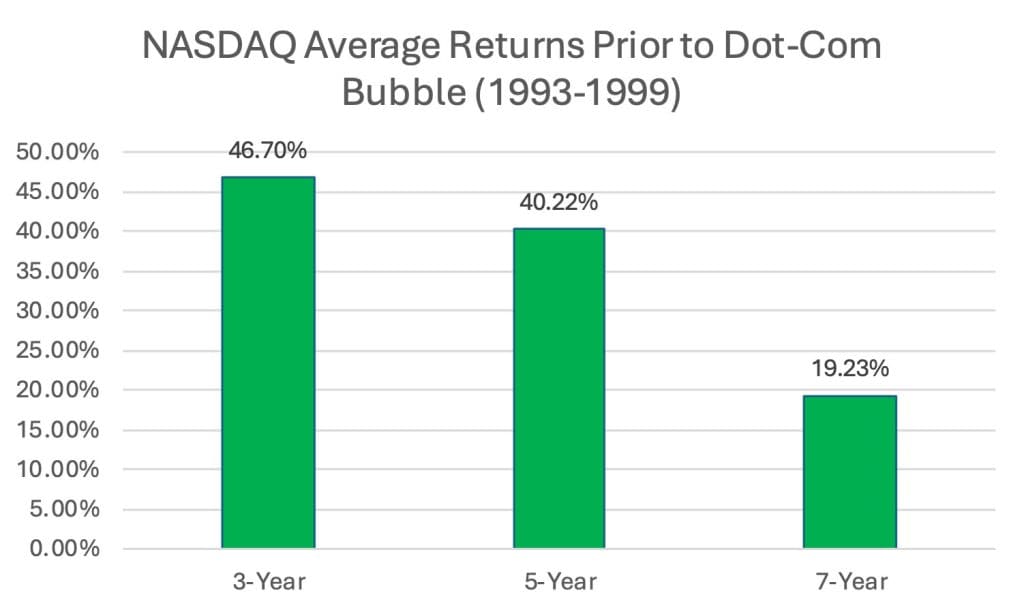

This is when historical average returns increase due to recent results. For example, at the end of 1999 the 3-, 5- and 7-year average returns of the NASDAQ increased considerably due to a few very good years. This led some investors chasing returns and abandoning more conservative, traditional allocations that might’ve been of higher quality:

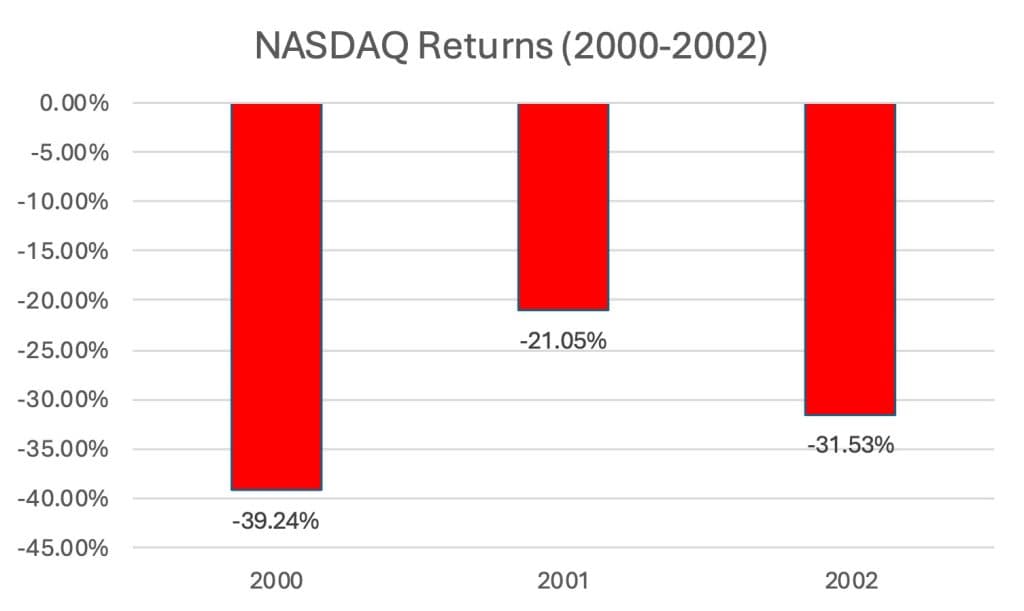

Source: Nasdaq Composite Index.Things looked very different looking at these averages in 2002:

Source: Nasdaq Composite Index. - Misconceptions About Sector Rotation

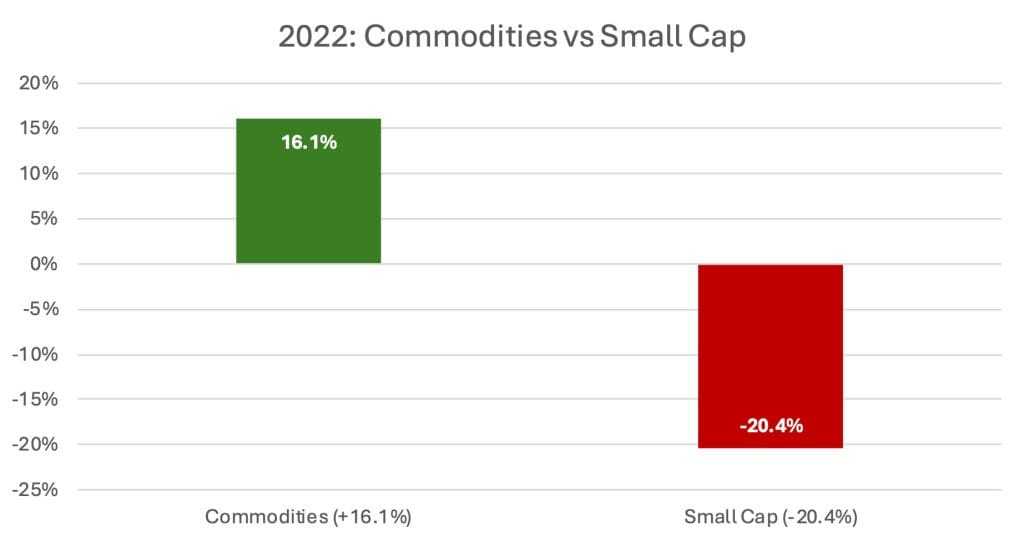

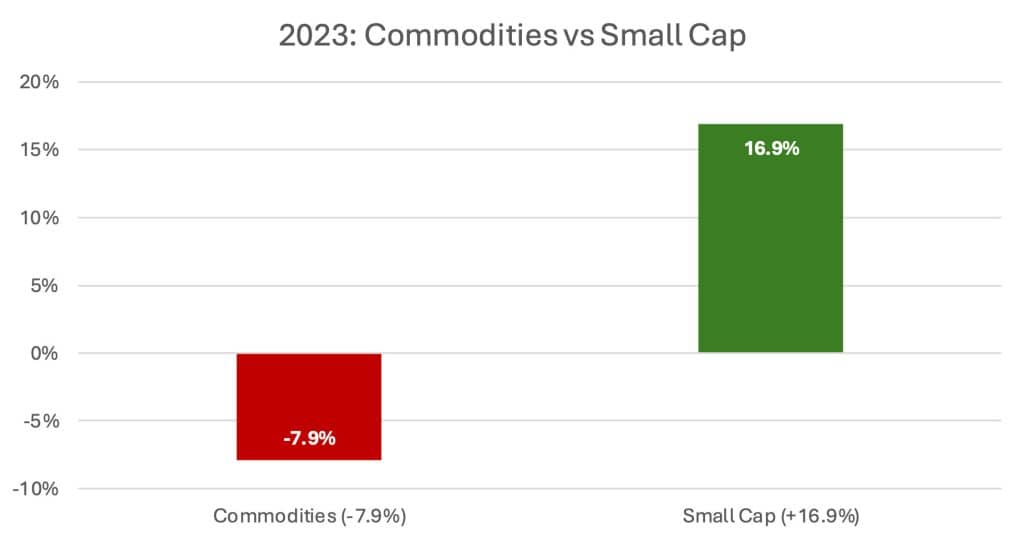

When investors spread risk across various sectors, they should know that each sector will rotate in and out of favor over time. This rotation in the short-term can lead to some sectors performing poorly while others do well. The challenge is that even the best Wall Street firms have been unable to predict which sectors are in favor or out of favor in any given year. Because of this, investors need to understand that long-term results are generated by time in the market, not timing the market. The below chart illustrates how quickly sectors can fall out of favor:

Commodity: Bloomberg Commodity Index, Small cap: Russell 2000

Commodity: Bloomberg Commodity Index, Small cap: Russell 2000

Poor Support

When investment advisors have limited support or licensing, they often charge a high fee only to sell products with hidden disadvantages. Because pooled investment products are packaged, evaluating the real cost, quality, turnover, size, and construction methodology can be difficult. Without adequate technology and staff, advisors are limited to a basic understanding of products’ past results without considering other factors.

It’s important to have a team of investment professionals working together to provide asset allocation, management, planning, and education, within a single investment firm. Unfortunately, many investment professionals focus on selling products rather than building a team to support the clients they already manage. Without a team, investment advisors end up wearing too many hats.

For example, equity managers are seldom talented in building a bond portfolio, and bond managers may not be good at financial planning or advising. With a comprehensive team, portfolios are constructed by bond and equity managers, advice and planning is done by skilled financial planners and advisors, and service is provided by a staff with quick communication. Without a full team of professionals, investors are often left wondering why they are falling short.

Related Articles

The Market Is Like a Coin—It Has Two Sides: Up and Down

Investment Principles,

Knowledge & Insights,

Markets,

Understanding Results,

September 17, 2024

Beginner Investment Mistakes to Avoid

Financial Planning,

Investment Principles,

Personal Finance,

Top Investor Mistakes,

June 24, 2024

What should I do if I am worried about the market?

Behavior,

Investment Principles,

Personal Finance,

Top Personal Finance FAQs,

October 1, 2024