By Indexopedia Research Team | October 1, 2024 | In

One of the biggest mistakes investors make is trying to time a down market. There are countless reasons why someone might be tempted to pull their money out or hesitate to invest. Maybe the market just hit an all-time high, there’s fear of an impending recession, concern over who’s in office, or anxiety about the national debt. The list goes on. While the reasons behind the fear may vary, history has shown that most investors, even the pros, cannot consistently time the markets. Even some of Wall Street’s most seasoned professionals have tried and failed.

So what should you do if you’re convinced the market is heading for a downturn?

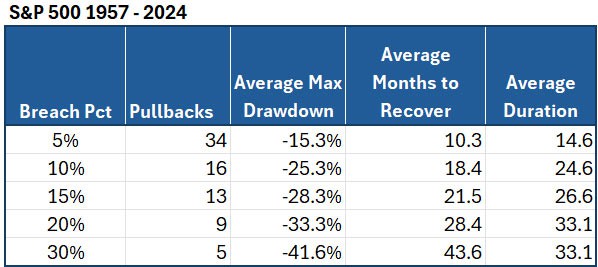

First, it’s important to understand that down markets, or pullbacks, are a natural part of market cycles. Much like breathing, the market inhales and exhales. Declines are just as much a part of the overall market cycle as the rallies. Over the last 67 years, there have been 34 market downturns ranging from -5% to -45%. That means, roughly half the time, the market is experiencing a pullback.

Exhibit 1 (Source: Factset)

Down markets aren’t a matter of if, but when. So, knowing that declines are inevitable, how should you invest when you think the market might drop? At Linden Thomas & Co., we believe in preparing for the worst-case scenario. Why? Because even if you don’t get the timing exactly right, you’ll be ready when the inevitable downturn arrives.

Unfortunately, many investors operate without considering the downside. They often put on their rose-colored glasses and invest when the market is strong, assuming those good times will continue indefinitely. But just like bad markets, good markets don’t last forever.

Two things to keep in mind:

- Just because the market is at a new high doesn’t mean a pullback is imminent.

- Similarly, just because there’s a pullback doesn’t mean the market won’t recover.

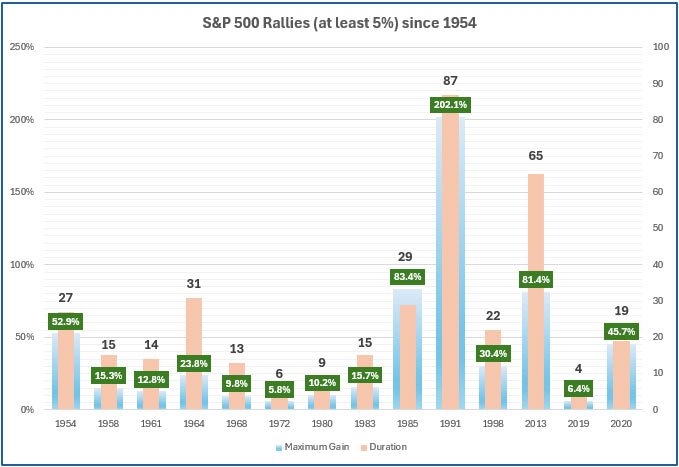

In fact, the market has hit countless new highs over the past decades, only to hit even more new highs soon after.

Exhibit 2 (Source: Factset. An index is unmanaged, and you cannot directly invest in an index)

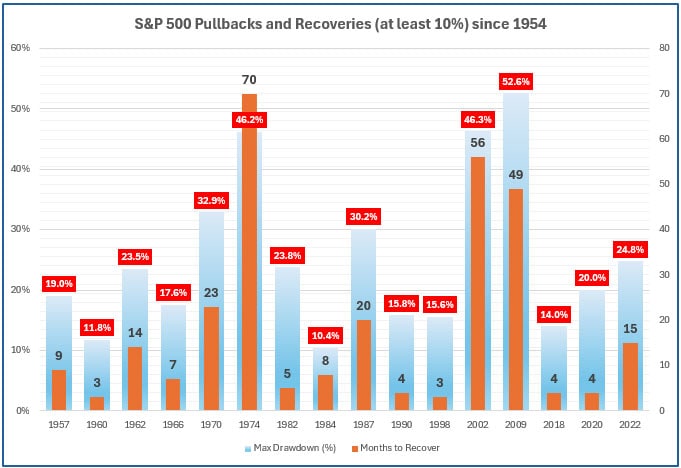

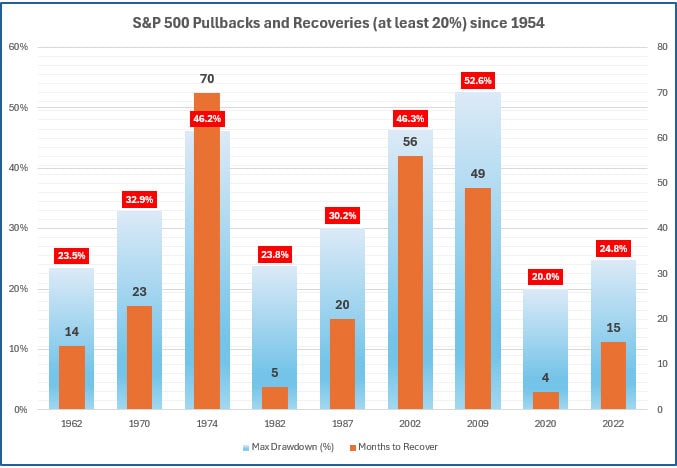

On the flip side, while pullbacks can be unnerving, history has shown that the market recovers. Take a look at how long it has taken the market to bounce back after a 10% or 20% pullback over the past several decades. (Exhibits 3 and 4):

Exhibit 3 (Source: Factset. An index is unmanaged, and you cannot directly invest in an index)

Exhibit 4 (Source: Factset. An index is unmanaged, and you cannot directly invest in an index)

So, assuming markets eventually recover, why doesn’t everyone just try to time the peaks, valleys, and recoveries? Simply put, because you can’t. Timing the market is nearly impossible. The market often moves in anticipation of events or lags behind them. If the market believes we’re headed for a recession, it frequently adjusts before the event materializes, pricing in potential declines in earnings. Conversely, when the market is down, it often begins its recovery before the external cause of the decline has been resolved.

A textbook example of this is 2020. At the onset of the COVID-19 pandemic, the S&P 500 sold off sharply by approximately -33%, but by year-end, they had bounced back by +60% (6% higher than the pre-pandemic high), even as COVID cases hit new highs. The market had recovered significantly, even though the pandemic was still raging. This is a prime example of why timing the market doesn’t work. Markets often overreact to events and then recover quickly, sometimes even while the news remains grim.

Even some of the brightest minds in finance have missed the mark when it comes to market timing. Consider the 2008-2009 financial crisis. Many of Wall Street’s top experts were wrong about when to exit or re-enter the market. Following their advice during the downturn could have been disastrous. Imagine your portfolio is down, and someone you respect advises you to sell to “protect what’s left.” You sell, only to realize a few months later that if you’d stayed the course, your portfolio would have fully recovered.

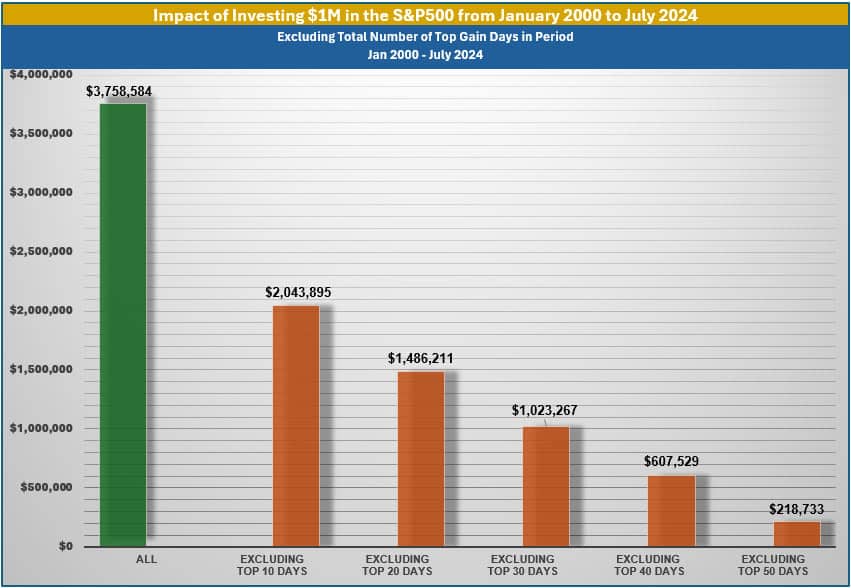

This is the challenge with market timing: markets rarely move according to your expectations. The media fans the flames, and Wall Street’s experts often miss the mark. And if you’re out of the market when the rally begins, missing just a few of the best days can significantly impact your long-term returns. (Exhibit 5 shows the impact of missing the top days from January 2000 to July 2024):

Exhibit 5 (Source: Factset. An index is unmanaged, and you cannot directly invest in an index)

So, what should you do if you’re still worried about the markets?

Invest based on your beliefs, but don’t try to time the market. If you’re conservative by nature or believe that the market is headed for a downturn, allocate your portfolio accordingly. But don’t base your strategy on the assumption that you’ll get the timing right. Instead, prepare for the possibility that you won’t–and make sure you can live with the results if you’re wrong.

Too often, investors don’t factor in the downside. When the market pulls back, they panic and sell, because they didn’t mentally or emotionally prepare for the decline. What was once a long-term investment goal becomes a short-term scramble to protect capital.

When allocating your money, always ask yourself: What happens if the market goes down? Can I handle that? Will I have the patience to stay invested long enough for a recovery?

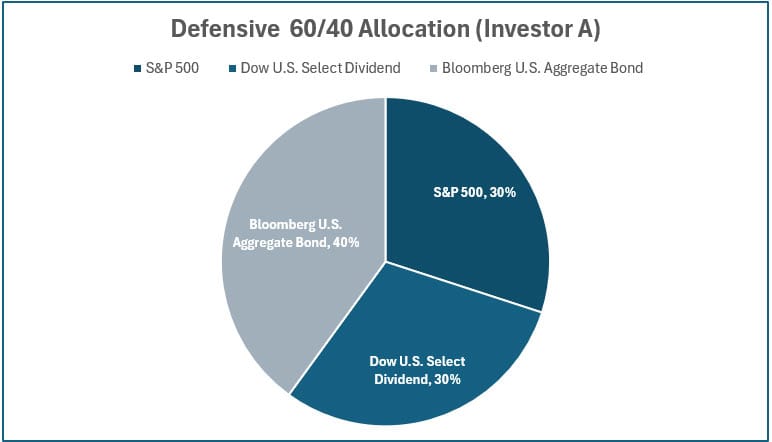

If you’re conservative, invest conservatively, but be prepared to miss out on some upside. Below, we illustrate two different investors. Investor A just sold his company for $20 million and wants to protect what he has. He’s also concerned about the economy and believes a market pullback is likely, so he invests defensively. (See Exhibit 6)

Exhibit 6 (Source: Zephyr. An index is unmanaged, and you cannot directly invest in an index)

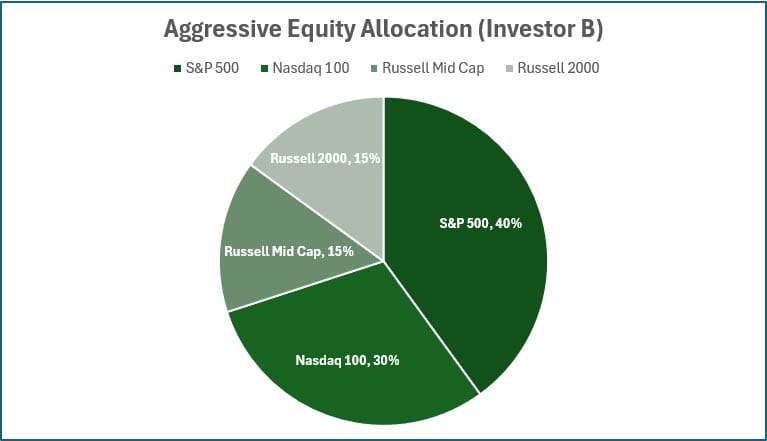

Meanwhile, Investor B is in his 50s and recognizes that markets fluctuate. He’s more comfortable with the market’s ups and downs and believes that holding mostly stocks will provide long-term rewards. (See Exhibit 7):

Exhibit 7 (Source: Zephyr. An index is unmanaged, and you cannot directly invest in an index)

While both investors have different approaches, each must understand the trade-offs between their strategies. Investor A, with his defensive posture, may see less volatility, but he’ll likely underperform the S&P 500 over the long term.

Pros and Cons of a Moderate Asset Allocation (Investor A)

- Pro: Potentially lower short-term risk

- Con: Potentially lower long-term returns

On the other hand, Investor B may see better long-term results, but his portfolio will experience more short-term volatility.

Pros and Cons of an Aggressive Asset Allocation (Investor B)

- Pro: Higher potential returns

- Con: Greater short-term uncertainty

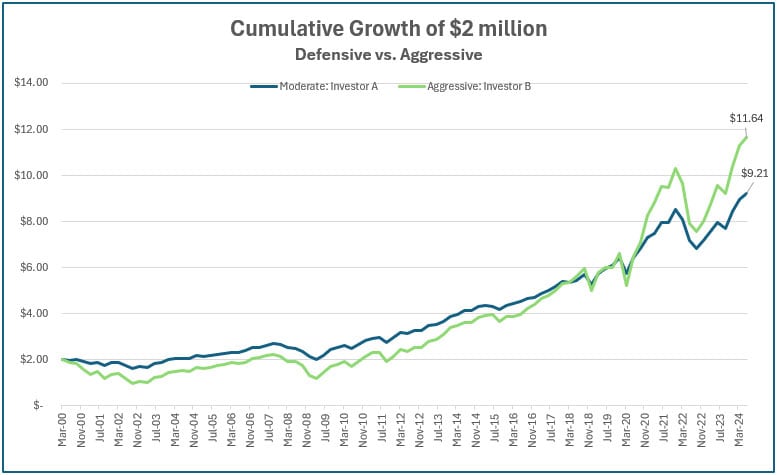

Each investor must be prepared to accept the consequences of their choices, both in the short and long term. As you can see below (Exhibit 8), from 2000 to 2024, Investor B outperformed Investor A over the long haul.

Exhibit 8 (Source: Zephyr. An index is unmanaged, and you cannot directly invest in an index)

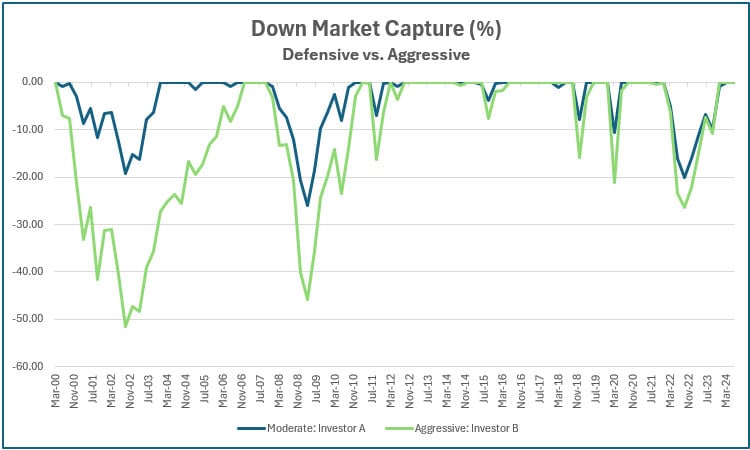

However, during market pullbacks, Investor A’s more conservative strategy cushioned his paper losses. (Exhibit 9)

Exhibit 9 (Source: Zephyr. An index is unmanaged, and you cannot directly invest in an index)

The key takeaway is that every investor needs to consider both the pros and cons of their approach. Conservative investors should remain conservative even when the market is up, and aggressive investors shouldn’t suddenly become conservative when the market pulls back. At Linden Thomas & Co., we believe in building portfolios tailored to each investor’s specific needs, starting with the understanding that markets will go down–it’s not a matter of if, but when. Like a coin, the market has two sides: highs and lows.

Remember, time in the market is more important than timing the market!

Related Articles

How Portfolio Overlap Could Be Putting Your Investments at Risk!

Financial Planning,

Investment Principles,

Personal Finance,

Top Investor Mistakes,

December 10, 2024

Rose Colored Glasses: Why Investing During the Good Times Can Create Poor Allocation Tilts

Investment Principles,

Top Investor Mistakes,

March 6, 2025

How Quality of the Portfolio Impacts Down Market Recovery and Compounding

Investment Principles,

Top Investment Principles FAQs,

January 15, 2025