Market downturns often trigger anxiety among investors, especially when they see bond prices declining. However, for those who own bonds directly rather than through mutual funds or ETFs, falling bond prices are not necessarily a cause for concern. In fact, they can present unique advantages that many investors overlook. Understanding the mechanics of bond investing can help investors stay the course and even capitalize on price declines.

The Yield Advantage: Higher Returns as Prices Drop

A key feature of bonds is the inverse relationship between price and yield. When bond prices fall, yields rise. This means that investors purchasing bonds during a downturn can lock in higher yields for the life of the bond, leading to increased future income.

Furthermore, if an investor already holds bonds, the coupon payments remain unchanged regardless of price fluctuations. These periodic interest payments provide a stable income stream, which can be reinvested into new bonds at lower prices, enhancing long-term returns.

Example: During the 2008 financial crisis, U.S. Treasury and corporate bond prices fell, pushing yields higher. Investors who purchased bonds during this period secured better income streams compared to those who invested in more stable market conditions. Over time, as the market recovered, bondholders also saw price appreciation alongside their locked-in higher yields.

Why Direct Bond Ownership Offers Stability

Unlike investors in bond mutual funds or ETFs, individuals who hold bonds directly have greater control and predictability over their investments. A bond held to maturity will repay its face value (barring default), regardless of interim market fluctuations. This eliminates the exposure to forced selling inside pooled bond funds.

The Risks of Bond Funds and ETFs in Down Markets

Investors in bond mutual funds and ETFs experience an entirely different reality during market downturns. These funds often face forced liquidations when investors redeem shares en masse (ie: small investor herding), compelling fund managers to sell bonds–even high-quality ones–at depressed prices. This process further exacerbates losses and can leave remaining investors with a weaker portfolio.

Example: In March 2020, during the initial COVID-19 market panic, many bond funds suffered massive redemptions. Fund managers had to sell bonds in an illiquid market, pushing prices down further. Meanwhile, individual bondholders who held their securities to maturity were able to ride out the volatility without realizing losses.

The Maturity Advantage: Predictability in an Uncertain Market

One of the greatest benefits of individual bond ownership is the certainty of principal repayment at maturity. Unlike stocks, which have no guaranteed floor, bonds (assuming the issuer remains solvent) will pay back their full face value at maturity, plus interest along the way. This provides a level of security that pooled bond funds or equities cannot offer!

Example: During the 2008 financial crisis, many high-quality corporate bonds saw temporary price declines. However, investors who held these bonds to maturity received their full principal back, in addition to earning their coupon payments throughout the downturn.

How Falling Prices Can Benefit Long-Term Bond Investors

Market sell-offs provide opportunities for bond investors to reinvest their income at higher yields. A well-structured bond portfolio allows for reinvestment as existing bonds mature or as coupon payments accumulate. This means that declining prices can be used strategically to increase future income.

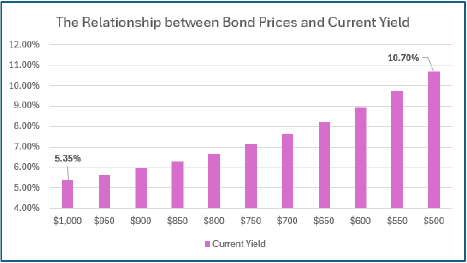

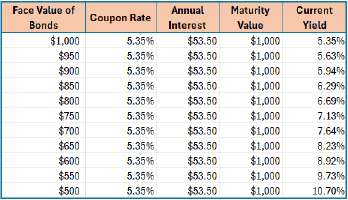

Example: Suppose an investor owns a $1,000 bond with a 5.35% coupon, earning $53.50 per year. If bond prices decline to $850 and the investor reinvests that $53.50 into new bonds offering 6.29% yields, their overall income stream improves over time. This compounding effect can significantly enhance long-term returns. The table and chart below demonstrate the inverse relationship between bond prices and current yield (see exhibit 1).

Exhibit 1

Conclusion

Investors should resist the urge to panic when bond prices decline. Those who own bonds directly enjoy predictable income, principal repayment at maturity, and the ability to reinvest at higher yields. Unlike bond mutual funds, direct bondholders avoid the pitfalls of forced liquidations and liquidity mismatches. Understanding these fundamental principles allows investors to approach market downturns with confidence and even turn declining bond prices into an opportunity for greater long-term gains.

Related Articles

Why Are Down Markets Your Friend?

Behavior,

Investment Principles,

Markets,

November 19, 2024

What Happens to Bonds in Down Markets? Should I Hold or Continue to Buy?

Fixed Income,

Top Fixed Income FAQs,

November 19, 2024

How Down Markets Can Actually Benefit Investments in Bonds and Dividend Stocks

Behavior,

Fixed Income,

Investment Principles,

Markets,

Why to Buy & Where,

August 14, 2024