By Indexopedia Research Team | March 6, 2025 | In

Teaching children about money is an investment in their future financial well-being. While many parents find it difficult to introduce financial concepts, early exposure helps build confidence and encourages responsible money management. From understanding the basics of saving to making informed investment decisions, financial education is a gradual process that evolves with age.

The following steps outline how to instill financial literacy at different stages of childhood and young adulthood.

1. Lay the Foundation Early

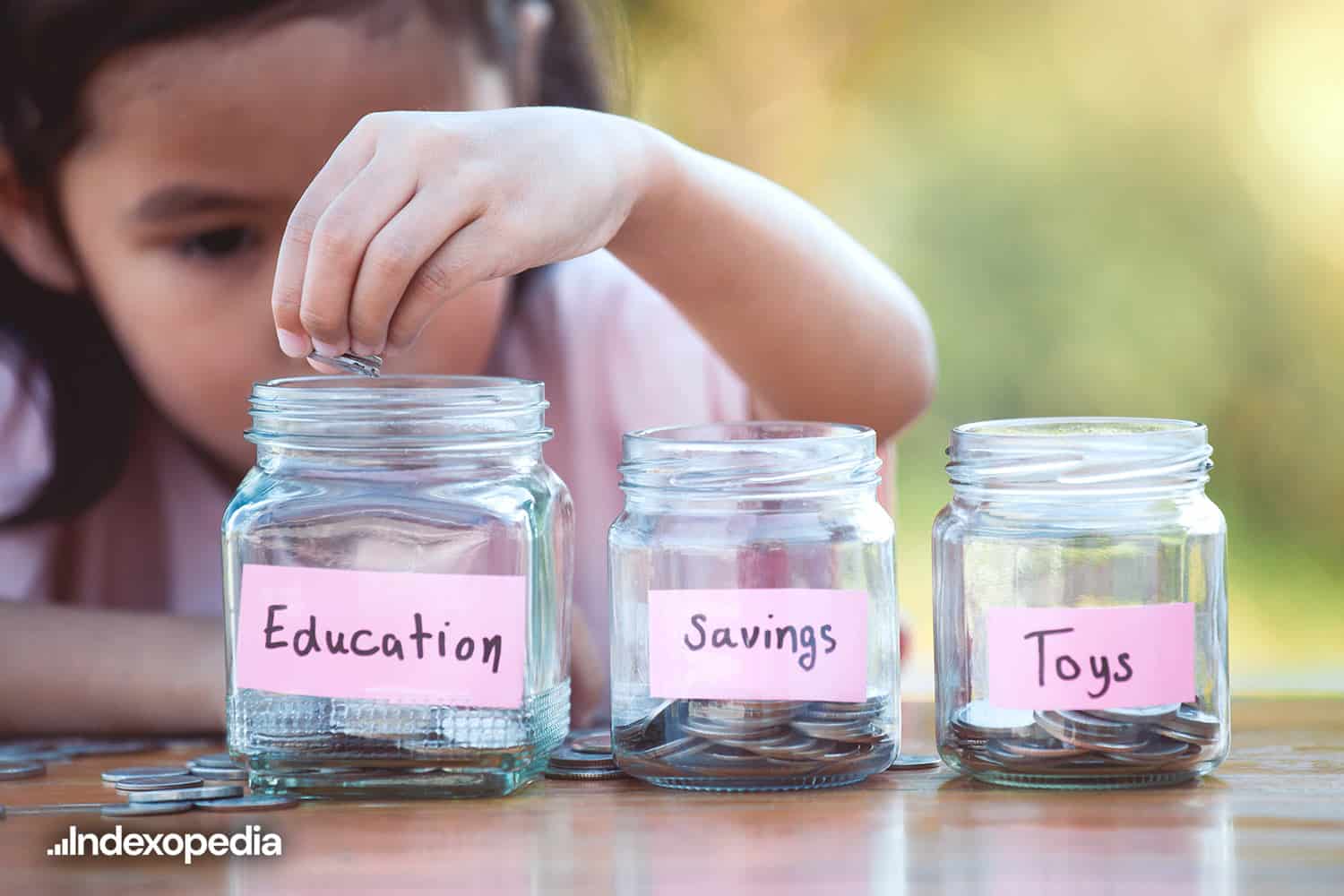

Financial habits begin forming at a young age, making early exposure to money concepts essential. Encouraging young children to handle physical money–such as coins and bills–helps them recognize its value. Using a piggy bank to store chore earnings or gift money introduces basic saving principles in a tangible way.

Opening a savings account around age five can reinforce these lessons. With parental guidance, children can participate in small banking tasks, such as making deposits or tracking their balance. Discussing spending decisions, distinguishing between necessities and luxuries, and setting aside a portion of savings for charitable giving can help shape responsible financial attitudes.

2. Introduce Investing Concepts

As children grow, introducing them to investing can help them understand how money can grow over time. One way to make investing relatable is by choosing well-known companies they recognize and guiding them through basic research on stock performance. Connecting financial concepts to real-life growth–such as comparing a company’s expansion to a child growing taller–can make the subject more engaging.

A hands-on approach, such as allowing a child to select and track their first investment, can build financial confidence. Learning how investments fluctuate and grow fosters long-term thinking and encourages them to view money beyond just spending and saving.

3. Use Rewards to Reinforce Good Habits

Encouraging children to save and invest is more effective when there are incentives. Some financial institutions offer rewards for making deposits, but parents can also introduce their own motivational strategies. Matching savings contributions or offering small bonuses for consistent saving can reinforce positive behaviors.

Introducing a Roth IRA when a child begins earning money–whether through an allowance, small jobs, or part-time work–can be a valuable long-term lesson. Parents can even contribute to the account to help instill the habit of setting money aside for the future. Seeing savings accumulate over time can make financial responsibility more appealing.

4. Increase Responsibility for Preteens and Teens

As children enter their preteen and teenage years, they should be given more control over their finances to help them develop real-world decision-making skills. Providing them with a set budget for a trip or personal expenses allows them to experience the impact of their choices. If they make an impulsive purchase and later regret it, the experience serves as a low-risk lesson in financial decision-making.

Opening checking and savings accounts during this stage introduces them to banking fundamentals, including the use of debit cards and the importance of monitoring balances. Teaching them about interest-bearing accounts can also help them understand how money grows over time.

5. Prepare Young Adults for Financial Independence

By the time children approach adulthood, they should be familiar with basic financial responsibilities. Parents can introduce budgeting by involving their teenagers in household financial discussions–without revealing every detail, but giving them insight into expenses such as rent, utilities, and grocery costs.

Encouraging college-bound students to take responsibility for personal expenses, such as entertainment subscriptions or discretionary spending, reinforces budgeting skills. Assisting with financial aid applications or discussing student loans can also help them understand long-term financial commitments.

This stage is also an ideal time to connect young adults with professional financial guidance. Learning about financial planning, wealth management, and the potential responsibilities tied to inheritances can provide valuable perspective before they step into full financial independence.

6. Put Safeguards in Place When Needed

Not every child develops strong financial habits right away, but safeguards can help ensure financial security. Trusts and structured financial plans can protect assets while allowing gradual access as young adults demonstrate responsibility.

Even if financial education starts later than ideal, it is never too late to introduce essential money management skills. Parents and financial professionals can play a crucial role in guiding young adults toward making informed, responsible financial choices.

By gradually increasing financial exposure and responsibility at each stage of childhood and young adulthood, parents can equip their children with the skills needed to navigate financial decisions with confidence.

Related Articles