By Indexopedia Research Team | January 8, 2025 | In

Fear and Greed are Not Your Friends

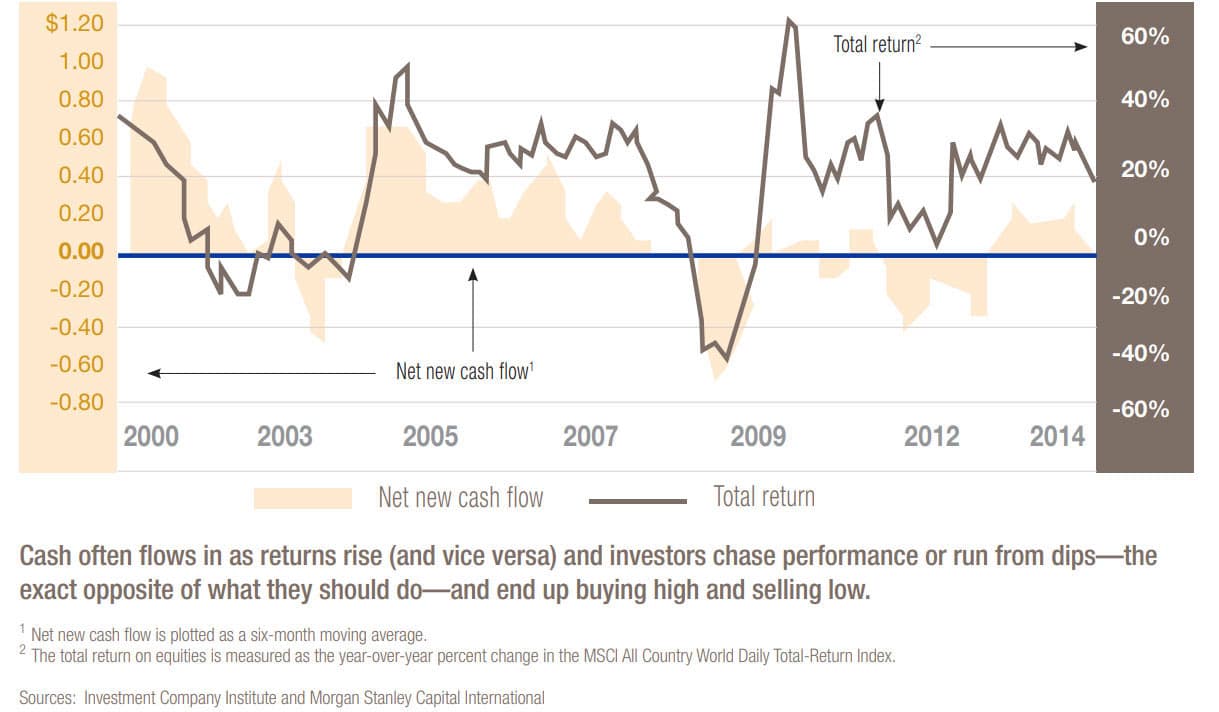

Two powerful emotions–fear and greed–often dominate decision-making, causing investors to act irrationally. While financial markets are driven by data, fundamentals, and trends, human emotions frequently derail logical thinking. To illustrate this point, the graph overlays annual market returns and the net new cash flow into stock mutual funds that occurred during, and surrounding, the market crash in 2009 (i.e., the amount individuals are investing, net of withdrawals).

New Cash Flow 2000-2014

As you can see, emotional investors tend to “buy high, sell low”, rather than following the age-old maxim of “buy low, sell high”. Powerful emotions like fear and greed can influence people and cause them to make irrational decisions. Bull markets can also cause some investors to abandon reason and common sense.

Fear

Fear arises when markets are volatile or when there’s a perception of impending losses. Investors may sell assets in a panic during market downturns, locking-in losses instead of riding out temporary fluctuations. This reaction stems from a desire to avoid further losses, but it can lead to missed opportunities when markets rebound. The investor often would be better off looking at down-markets as an opportunity to add to their portfolio at a discount.

One of the most recent examples of this was the massive selling of stock funds during the credit crisis that began in 2008. Investors who “cut and ran” over-invested in cash, creating purchasing power risk. Not only did they sell at an inopportune time, many remained out of the market waiting for “the right time” to redeploy assets, and consequently missed the price recovery that began in March of 2009. Attempting to time when to buy and sell creates two opportunities to get it wrong.

Risk aversion is the tendency for investors to prioritize safety over potential returns, often choosing lower-risk investments to avoid the possibility of losses. While this cautious approach can protect against significant downturns, it can also limit growth, as lower-risk assets typically offer lower returns over time. Investors who are highly risk-averse may miss out on opportunities for wealth accumulation, especially in the long term. Balancing risk aversion with appropriate exposure to higher-growth assets is key to achieving a well-rounded investment portfolio. Understanding one’s risk tolerance is crucial for making decisions aligned with both financial goals and emotional comfort.

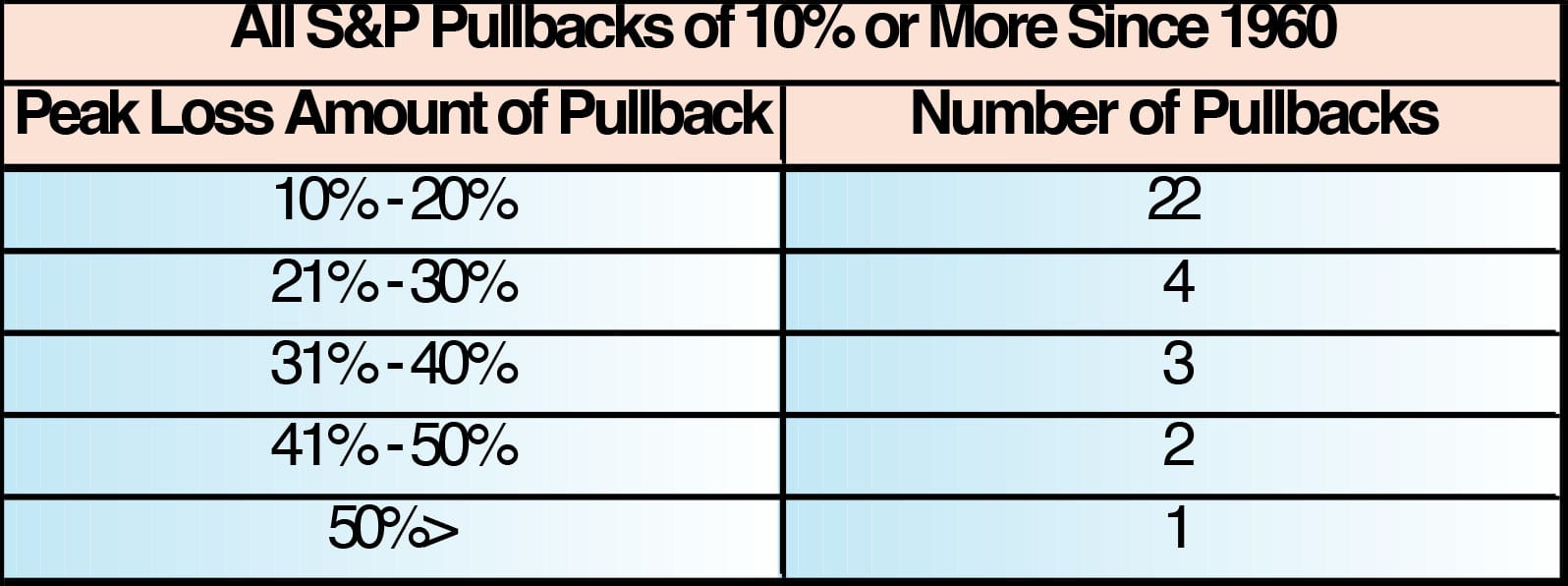

From 1963-2021 there were 32 S&P 500 pullbacks of 10% or more. While no one likes down-markets, it’s important to understand that it is like breathing. Breathing consists of two actions: inhaling and exhaling. No one ever walked the earth without doing both. This is also true in investing. If you own stock in any healthy company, the long-term increase in value fluctuates between rallies (inhale) and pullbacks (exhale).

Source: S&P 500

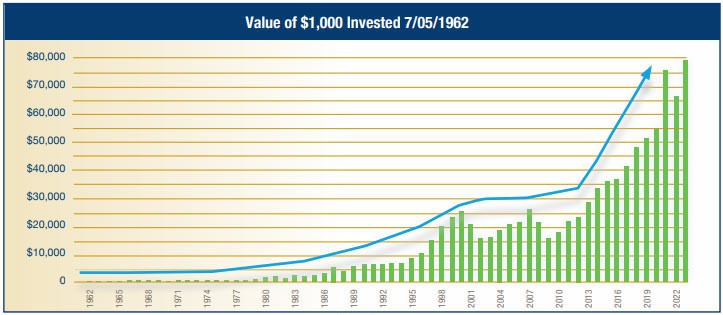

Even with all this volatility, those who were patient created wealth. The chart below shows how $1,000 invested in the S&P in 1962 became $78,275 by 2023. In fact, you’d have much more than $78,275 if you had the discipline to add during the dips and reinvest dividends. Unfortunately, market dips are often accompanied by bad news, which can create even more fear. Often bad markets accompanied by bad news will make us believe that things can only get worse.

Out of the 63 years shown below, all but 13 of them experienced a pullback greater than -10% or were still recovering from a prior pullback. Long recoveries can be frustrating but wise investors see an opportunity to accumulate shares at a discount. Remember: shares are more important than value. The value of a portfolio fluctuates, but the number of shares doesn’t. For those that don’t have investable capital, or don’t have the wisdom to add to their shares, long recoveries can create bad behaviors and poor results. Two such recoveries began in 2002 and 2009. Both of these recoveries were prolonged and accompanied by ongoing bad news which scared investors that didn’t proactively add to their portfolio.

Source: S&P 500.

History has proven that even while the recovery is taking place, bad news is still prevalent. This is because the market is forward-looking. If the market feels that future or current events will create a recession or result in poor earnings, then the market often ‘bakes-in’ those effects. In the short-term, the market can overreact to bad news, but long-term effects are priced-in in advance. Over time, markets are usually moving towards a fair price, while in the short-term volatility can create doubt and fear.

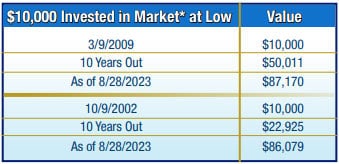

While some recoveries take time, they are often followed by some of the best rallies. One such moment followed the 2007-2009 banking crisis. After the -49% market correction from October of ’07 to November of ’09, investors’ principal did not recover until March of 2013. Yet from the end of 2012 to the end of 2021 the market returned an unbelievable 13.99% annualized. Many severe downturns are followed by the best markets in history. If you have the discipline to stay invested or add to your position during these times, history has proven that you will be rewarded. Below illustrates how a small investment of $10,000 invested during the dips of 2002 and 2009 increased more than eight-fold.

Source: S&P 500 Total Return.

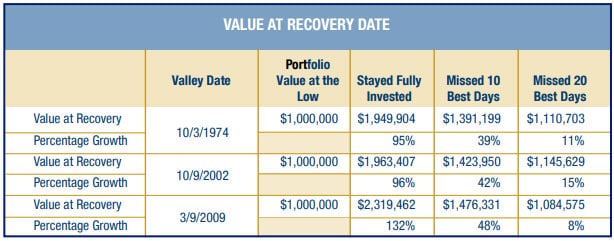

While staying invested can be tough, history has proven that it’s rewarding. It is tragic to see investors experience a full or partial downturn, wait for good news to reinvest, and then miss out on most of the recovery. In the three examples below, the investor would be missing out on substantial returns if they missed the top 10 or 20 days of a recovery. Because the markets are forward looking, pullbacks often happen before the really bad news is out, but recovery takes place when the news is at its worst. Why? Because the market often bakes-in the worst-case scenario. When the worst-case scenario doesn’t take place, the oversold equities rally to recovery.

Source: S&P 500.

Many investors only return to the markets once the media says things are getting better, but by the time you hear about the good news much of the recovery has already happened. Investing during U.S. election years can amplify the influence of fear and greed, as uncertainty surrounding political outcomes often triggers heightened market volatility. Historically, election years bring speculation about changes in policies, regulations, and taxes, which can impact sectors differently based on the anticipated winner. This uncertainty can lead investors to make hasty decisions, either pulling out of the market out of fear of unfavorable policies or rushing to invest in sectors they believe will benefit from the election result. However, long-term data shows that markets generally recover from election-year jitters, regardless of the outcome. To avoid letting emotions dictate decisions, investors should focus on their broader financial strategy, maintaining a long-term perspective while avoiding reactions to short-term political noise. Staying diversified and relying on historical trends, rather than speculation, can help investors navigate market cycles more confidently.

During periods of negative headlines and doomsday-like predictions from “experts”, the market always bounces back. When the market is in a decline, it’s important to recall how resilient financial markets are. Take a look at how substantially the S&P 500 recovered from financial panics:

Source: S&P 500.

Greed

Greed, on the other hand, occurs when markets are thriving, and investors feel the urge to maximize profits. In times of euphoria, people may buy into overvalued assets, believing they will continue to rise. This overconfidence can lead to bubbles, where the eventual correction can cause severe financial harm.

Nobel Prize winner and behavioral finance expert Daniel Kahneman developed what is known as “prospect theory”, which holds that individuals are more likely to be influenced by short-term volatility, even if they are pursuing a long-term strategy. This is exacerbated by the recency effect; a psychological phenomenon that causes people to place too much importance in the most recent results.

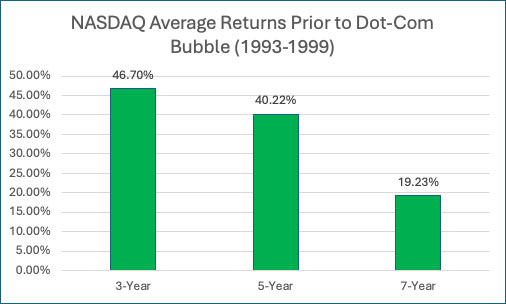

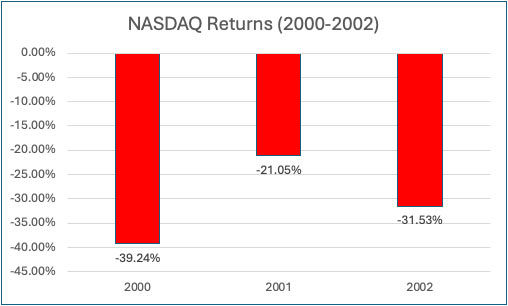

This bias towards the most recent information is amplified by common misunderstandings of average returns. When an asset class, sector, or even individual stock moves up it increases the trailing average returns. As an example, below you can see how the rise of the dot-com bubble influenced the NADAQ average returns:

Source: Nasdaq Composite Index.

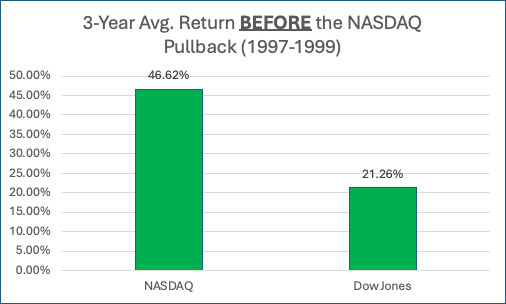

This led some investors to abandon out-of-favor traditional sectors like value and blue-chip stocks. Investors moved into dot-coms with the belief that growth will never diminish. There are many examples of this behavior in the past, like biotech, dot-coms, technology, gold, and bitcoin. After the three-year NASDAQ rally during 1997-1999 that looked much different than the three years from 2000-2002.

Source: Nasdaq Composite Index.

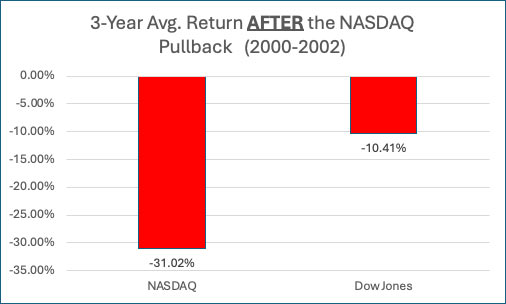

As seen below, the Dow Jones did not perform as well as the NASDAQ during the rally, but it performed better than the NASDAQ during the pullback. This is another one of the reasons to keep a diversified portfolio. In any given year, it is impossible to determine which asset will be the best performer. By having exposure to various indices and asset classes, you can avoid the damage that comes from putting all of your eggs in one basket.

Source: Nasdaq Composite Index & Dow Jones Industrial Average.

All too often, average return results after a rally make investors believe they have failed to fully participate. If you have only a small percent in the successful sector, then average returns might convince you to increase your allocation to these assets. Over time, this behavior can prove to be very damaging to one’s long-term results. Greed and fear are not your friends, but balance and time are.

With institutional direct indexing, investors can customize their portfolio, allowing for greater control and flexibility. This means that during a market downturn, investors can strategically sell underperforming stocks, harvest tax losses, or adjust exposure to specific sectors that they believe will recover more quickly. Additionally, direct indexing enables investors to tailor their portfolio to align with personal values or financial goals, potentially offering more targeted downside protection than a standard index fund. By evaluating the earnings-quality of the companies in the index, direct indexing investors can add another layer of confidence to their investment strategy.

Both fear and greed distort an investor’s judgment, leading to impulsive buying and selling. To avoid falling into these traps, it’s crucial to have a disciplined strategy, focusing on long-term goals rather than short-term market movements. Warren Buffett, perhaps the greatest investor of all time, has said, “be fearful when others are greedy, and greedy when others are fearful”. Following the herd is a good way to sabotage an otherwise solid long-term strategy.

Related Articles

The Market Is Like a Coin—It Has Two Sides: Up and Down

Investment Principles,

Knowledge & Insights,

Markets,

Understanding Results,

September 17, 2024

The Media’s Role in Fueling Market Hysteria: Lessons for the Prudent Investor

Behavior,

History of Markets,

Investment Principles,

Markets,

September 19, 2024

What should I do if I am worried about the market?

Behavior,

Investment Principles,

Personal Finance,

Top Personal Finance FAQs,

October 1, 2024